How frail are the firms?

Business Standard, 11 December 2007

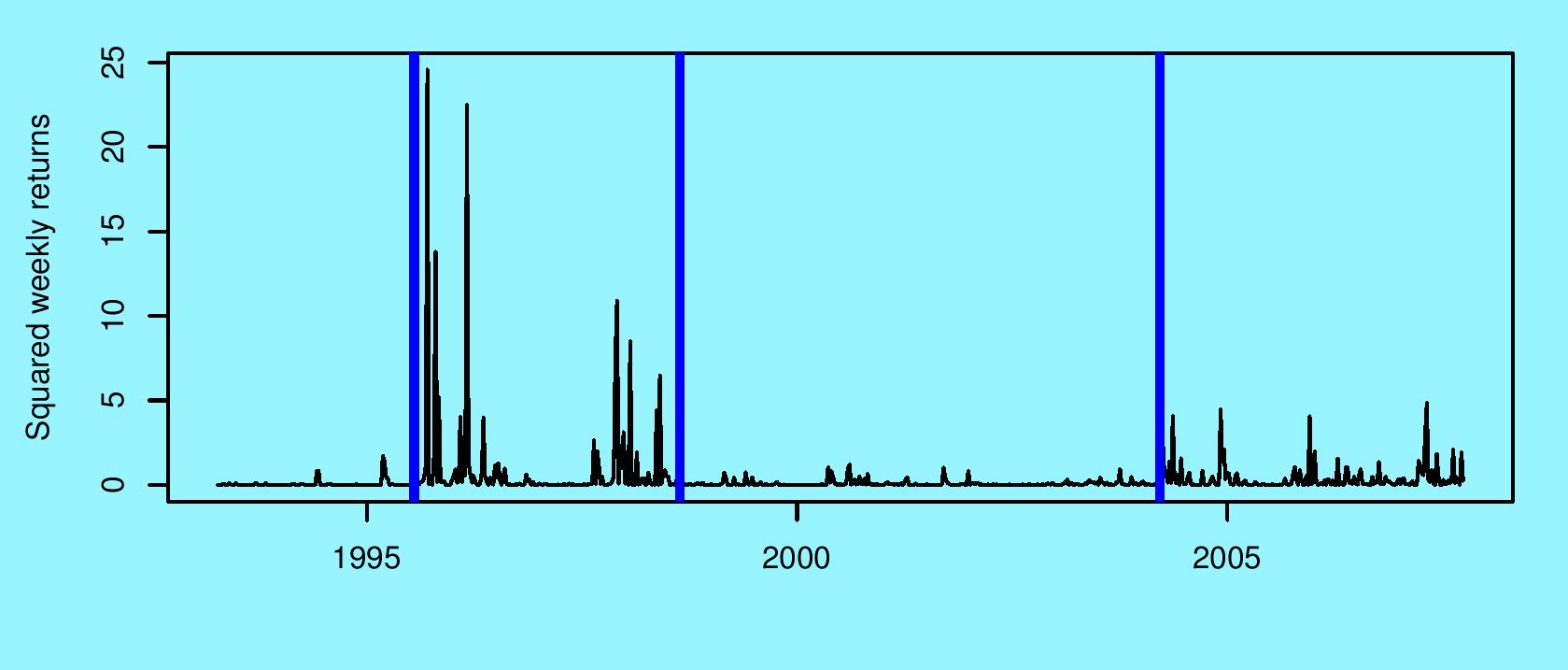

Recent developments in thinking about exchange rate regimes offer an useful characterisation of India's evolution in this regard. India has gone through four phases, with low (1993-95), high (1995-98), low (1998-2004) and then high (post-2004) exchange rate flexibility. This is a natural experiment in which we can observe the evolution of the currency exposure of Indian firms. The evidence strongly suggests that firms take on more currency risk when exchange rate flexibility is lower.

The first research meeting of the NIPFP-DEA Research Program on Capital Flows and their Consequences had a fascinating set of research papers on the interlinked subjects of capital controls, the exchange rate regime and monetary policy. One area of exploration was the exchange rate regime and its consequences.

There has been a pattern, worldwide, where the exchange rate regime actually in operation differs from what is officially claimed. This has motivated a quest for data-driven schemes for identifying the exchange rate regime that is actually in operation. While many schemes have been proposed, they often disagree with each other, and sometimes tend to rely on rules of thumb in classification.

A workhorse of this literature is the `exchange rate regression' where fluctuations in the rupee are explained using fluctuations in the dollar, the pound, the euro and the yen. If the rupee is pegged to the dollar, the coefficient of the dollar will be near 1 and the residual volatility will be low.

In recent work, Achim Zeilies of Vienna University, Ila Patnaik and I approached this question from a fresh perspective. Since the exchange rate regime is evolving through time, a natural idea is to examine this regression using the tools of structural change. We extend standard tools of structural change to suit the needs of this problem, and obtain a consistent strategy for testing, dating and monitoring exchange rate regimes.

In the Indian case, this methodology identifies four phases of the exchange rate regime. The first ran from April 1993 to March 1995. It was a tight USD peg with a residual volatility of 0.16% per week. The second phase ran from March 1995 to August 1998. It was also a USD peg, with the highest residual volatility of 0.92% per week. The third phase was from August 1998 till March 2004 - this was essentially a USD peg with a low residual volatility of 0.28% per week.

In the Indian case, this methodology identifies four phases of the exchange rate regime. The first ran from April 1993 to March 1995. It was a tight USD peg with a residual volatility of 0.16% per week. The second phase ran from March 1995 to August 1998. It was also a USD peg, with the highest residual volatility of 0.92% per week. The third phase was from August 1998 till March 2004 - this was essentially a USD peg with a low residual volatility of 0.28% per week.

We are now in the fourth phase, which commenced in March 2004, where some signs of influence from other currencies are found, and the residual volatility is higher at 0.58% per week. Yet, this is lower than the currency flexibility that India had experienced in the second phase.

This natural experiment - where exchange rate flexibility went through three changes - offers an opportunity to examine what happened to the firms. There are two views on this question.

One view -- the "incomplete markets hypothesis" -- holds that firms are helpless. The currency derivatives market is weak, capital controls prevent the firms from managing their own exchange rate risk, firms are not as thoughtful as they should be in thinking carefully about that risk and the non-transparency of RBI implies that the firms are in the dark. This view suggests that these frailties of firms require a public sector risk management solution: the government should prevent exchange rate volatility because the firms need this protection.

One view -- the "incomplete markets hypothesis" -- holds that firms are helpless. The currency derivatives market is weak, capital controls prevent the firms from managing their own exchange rate risk, firms are not as thoughtful as they should be in thinking carefully about that risk and the non-transparency of RBI implies that the firms are in the dark. This view suggests that these frailties of firms require a public sector risk management solution: the government should prevent exchange rate volatility because the firms need this protection.

The alternate view -- the "moral hazard hypothesis" -- holds that firms are smarter and more resourceful than we think. Firms are able to outsmart capital controls, and even though currency derivatives are weak, they are able to modify their currency exposure. Firms are smart and understand what currency risk is all about. In this view, firms exploit the frailties of the government and make money off one-way bets, or free risk management, given out by pegged exchange rates.

Ila Patnaik and I analyse the data for Indian firms, across this natural experiment of low-high-low-high exchange rate flexibility, to see which of these two views is supported by the evidence.

We focus on the 100 firms in Nifty and Nifty Junior - the most liquid and efficient markets in the country, where speculators are actively looking at all kinds of information about firms and impounding them into the publicly visible price. We measure exchange rate exposure through the stock price. We ask what is the change in the stock price (on average) for a 1% change in the exchange rate. As an example, for Satyam Computers, we find that the stock price gains 2.44% when there is a 1% depreciation in the INR/USD exchange rate. This suggests that Satyam has a currency exposure in the direction of losing when the rupee appreciates.

Such measurement of exchange rate exposure is trusted because speculators on the stock market have an incentive to look at all kinds of risk: economic risk, off-balance sheet exposures, currency derivatives, etc. that the firm may have in place. If Tata Steel loses profitability when a rupee appreciation leads to a lower price for steel in rupees, the stock market sees this, and it would show up in our measurement.

Some exposures are positive - as with Satyam - where a stock price goes up with a depreciation. Others are negative. In order to focus on the risk exposure of firms, we focus on the absolute value of exposure, disregarding the sign.

The findings are striking. In the first period - with the lowest currency flexibility - the average exposure was 12.59. In the second period - with the highest currency flexibility - exposure dropped to 1.04. In the third period, with low flexibility, exposure went back up to 3.45. Finally, in the fourth period, with greater flexibility, exposure dropped to 1.49. In addition, we also find that the Indian corporate sector - as a whole - has a statistically significant bet on rupee exposure in the fourth period. For all the complaints of CEOs about rupee appreciation, the stock price processes of Nifty and Nifty Junior companies show gains (on average) when INR/USD appreciates.

This evidence is particularly striking because RBI makes no announcements about the exchange rate regime in operation. Until sophisticated econometrics was put into play, these dates of phases of the exchange rate regime were not known. Yet, the firms were able to intuitively sense what was afoot, and dodge capital controls, so as to get their optimising responses in place. Lower financial fragility requires greater currency volatility.

Back up to Ajay Shah's 2007 media page

Back up to Ajay Shah's home page