Fix both distortions together

Business Standard, 16 January 2007

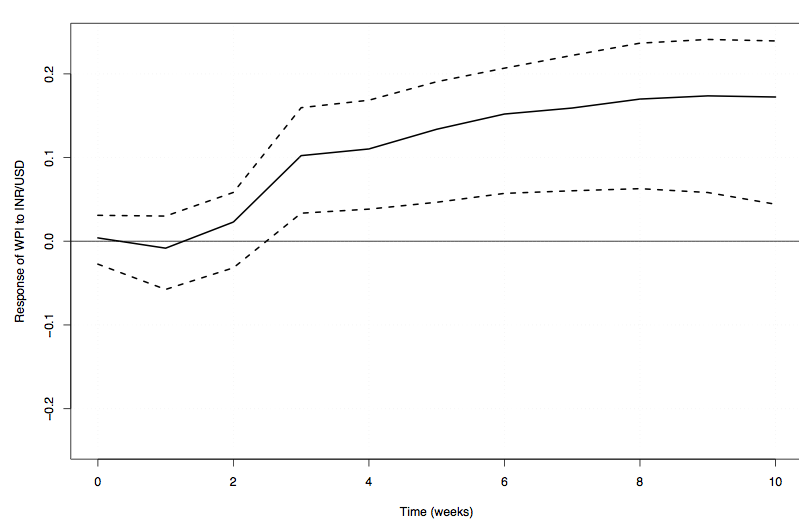

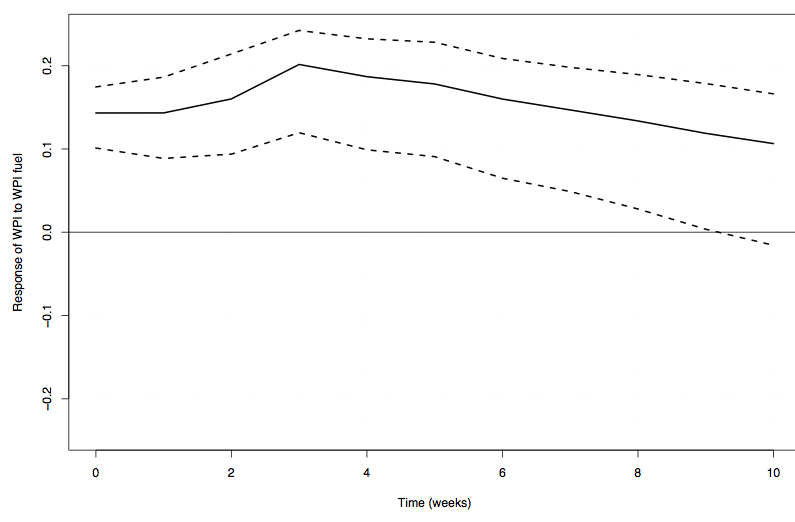

There are two key controlled prices in India: the rupee-dollar exchange rate and the prices of petroleum products. In both cases, the process of market price adjustment is held back by the government. As a consequence, the apparent inflation of the economy is wrongly perceived in the standard data. Some estimates of the relationships are as follows. A change in the INR/USD impacts on the overall WPI: a 1% depreciation of the rupee shows up in the third week with a 0.1% rise in WPI, going till a 0.15% rise in the 10th week. A 1% rise in the WPI fuel gives an immediate impact of 0.15% in the WPI, going up to 0.2% in the 3rd week, and tapering off in roughly 10 weeks.

While the role of the government in fixing prices in the economy has diminished over the years, two key areas where government makes decisions are the rupee-dollar exchange rate and the prices of petroleum products.

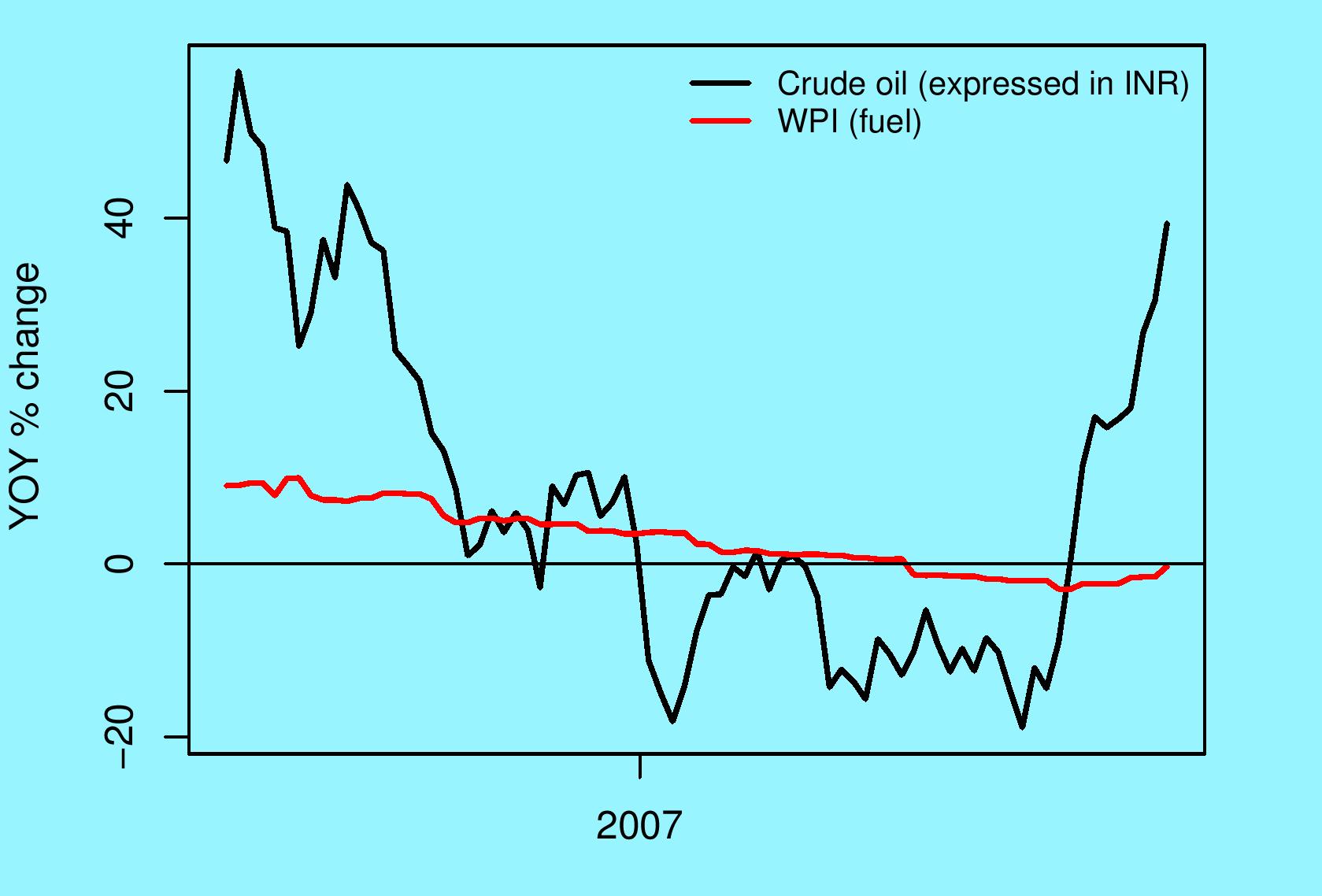

In the case of the WPI Fuel, the latest data shows a zero change in WPI Fuel on a year-on-year basis. The price of the `Indian basket' of crude oil, expressed in rupees, shows a 40% rise when compared with a year ago. (See figure on the right). This suggests that there is a pent up need for an increase in petroleum products.

In the case of the WPI Fuel, the latest data shows a zero change in WPI Fuel on a year-on-year basis. The price of the `Indian basket' of crude oil, expressed in rupees, shows a 40% rise when compared with a year ago. (See figure on the right). This suggests that there is a pent up need for an increase in petroleum products.

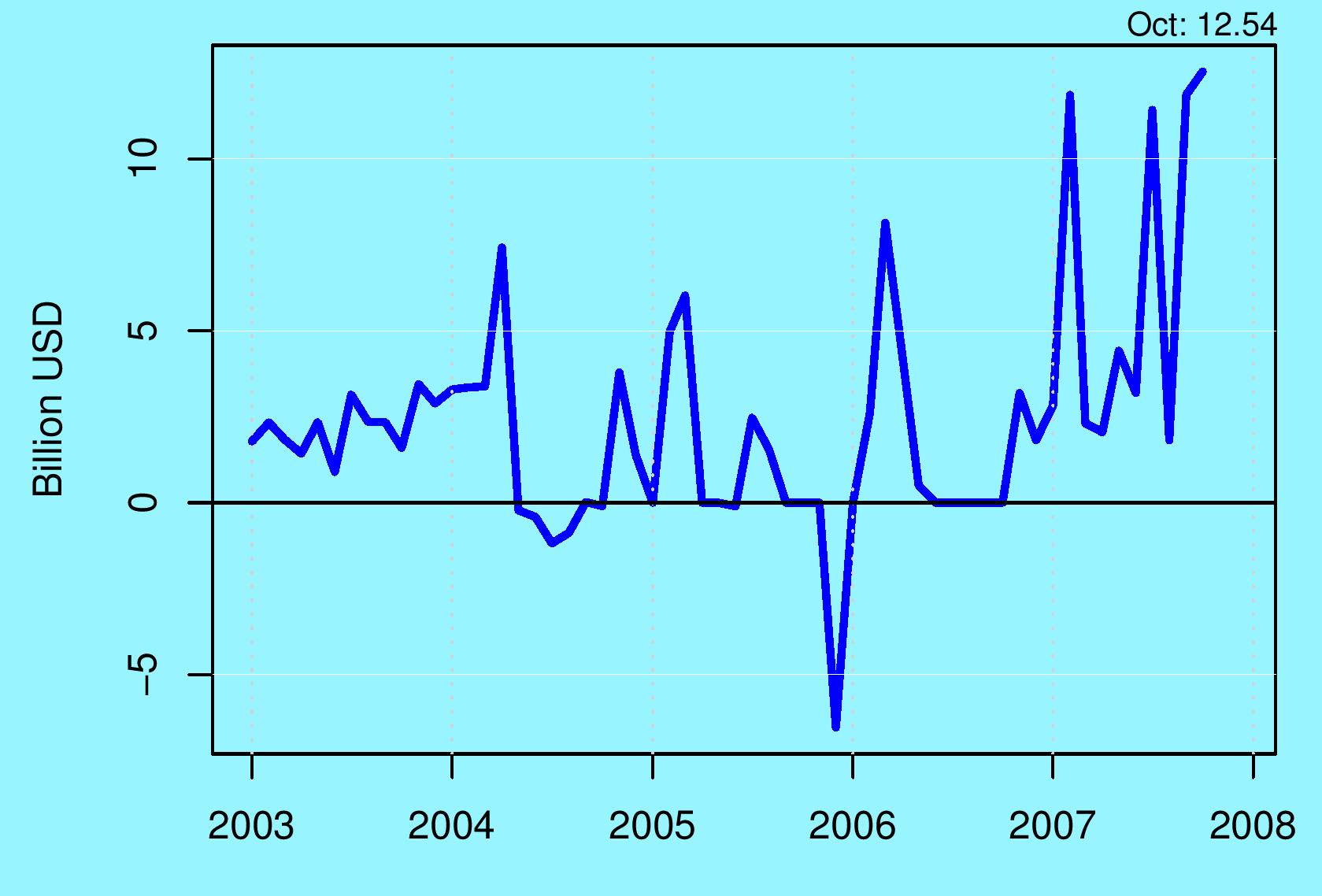

In similar fashion, the RBI has engaged in massive and unprecedented purchases of dollars in September and October (roughly $12 billion a month). (See figure on the right). This suggests that there is a pent up need for an appreciation of the rupee.

In similar fashion, the RBI has engaged in massive and unprecedented purchases of dollars in September and October (roughly $12 billion a month). (See figure on the right). This suggests that there is a pent up need for an appreciation of the rupee.

When the government is preventing market forces from operating in these two areas, the standard inflation data is faulty. When the rupee is prevented from appreciating against the USD, prices of imported goods are exaggerated, and the apparent inflation is overstated. The footprint of the exchange rate is bigger than meets the eye, because many local transactions are priced at world prices in what is called `import parity pricing'. When the global rise in oil prices is not passed on into local prices of petroleum products, prices of fuel are artificially kept down, and the apparent inflation is understated. In order to think effectively about these questions, quantitative estimates of these effects are required.

The relationships under examination - such as the extent of import parity pricing in the economy - have been evolving over the years. For example, when customs duties come down and infrastructure gets better, the extent of import parity pricing goes up. Hence, we set about doing this using weekly data from July 2002 onwards. This recent period is utilised in order to capture the recent nature of the relationships. In all cases, the inflation data that is analysed is the year-on-year percentage change.

In the case of the exchange rate, a 1% depreciation (on a yoy basis) of the rupee-dollar exchange rate initially has no effect on the yoy change in WPI. The first statistically significant effect - of roughly 0.1% - shows up with a lag of 3 weeks. This effect slowly enlarges, reaching a value of 0.15% by the 10th week. The impact is statistically significant beyond 10 weeks also. (See impulse response function, with 95% confidence interval, on the right).

In the case of the exchange rate, a 1% depreciation (on a yoy basis) of the rupee-dollar exchange rate initially has no effect on the yoy change in WPI. The first statistically significant effect - of roughly 0.1% - shows up with a lag of 3 weeks. This effect slowly enlarges, reaching a value of 0.15% by the 10th week. The impact is statistically significant beyond 10 weeks also. (See impulse response function, with 95% confidence interval, on the right).

These effects work in reverse, of course, with an appreciation of the rupee-dollar. A 10% rupee appreciation would yield reduced yoy WPI inflation to the tune of 1 percentage point by the 3rd week going to roughly 1.5 percentage points by the 10th week.

Petroleum products are a sub-component of WPI Fuel. Petrol makes up 6.2% of the WPI Fuel, kerosene is 4.8% and HSD is 14.2%. While these are significant weights, it is important to remember that WPI Fuel is much more than the controlled prices for petrol, kerosene and HSD.

We find that a 1% rise in WPI Fuel, on a yoy basis, yields an immediate impact of roughly 0.15%, going up to 0.2% in week 3. After this, the size of the effect tapers away, losing statistical significance by the 9th week. (See impulse response function, with 95% confidence interval, on the right).

We find that a 1% rise in WPI Fuel, on a yoy basis, yields an immediate impact of roughly 0.15%, going up to 0.2% in week 3. After this, the size of the effect tapers away, losing statistical significance by the 9th week. (See impulse response function, with 95% confidence interval, on the right).

There are interesting differences between the impact of a change in the INR/USD exchange rate against the impact of a change in WPI Fuel. In the latter case, there is an instant effect, while the INR/USD has no impact in the first two weeks. The WPI Fuel generates a bigger impact of 0.2% in the third week. But the impact of the WPI Fuel rapidly fades away and is statistically insignificant by the 10th week. In addition, there is no statistically significant impact of the WPI Fuel on the CPI-IW.

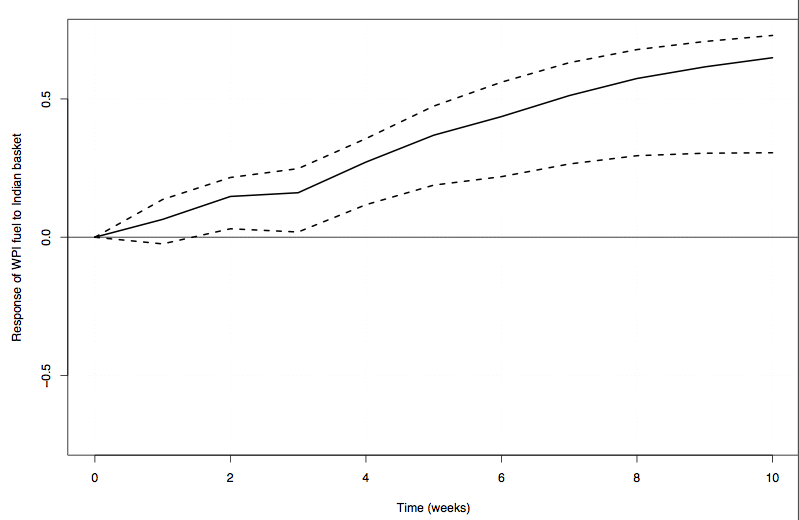

This strategy for data analysis can also be applied to understanding the behaviour of the politicians when it comes to changes in WPI Fuel. When the price of the Indian basket of crude oil, expressed in rupees, is 1% higher on a yoy basis, what happens to WPI fuel? The evidence shows that roughly nothing happens for three weeks, but a statistically significant impact is visible from week 4 to week 10. By week 10, the size of the impact is roughly 0.6. This gives us an idea about the lags in the behaviour of administered prices, on average. The story on the government's decisions on the rupee-dollar pegged exchange rate is more complex, where the primordial urge to peg comes into conflict with monetary policy distortions.

This strategy for data analysis can also be applied to understanding the behaviour of the politicians when it comes to changes in WPI Fuel. When the price of the Indian basket of crude oil, expressed in rupees, is 1% higher on a yoy basis, what happens to WPI fuel? The evidence shows that roughly nothing happens for three weeks, but a statistically significant impact is visible from week 4 to week 10. By week 10, the size of the impact is roughly 0.6. This gives us an idea about the lags in the behaviour of administered prices, on average. The story on the government's decisions on the rupee-dollar pegged exchange rate is more complex, where the primordial urge to peg comes into conflict with monetary policy distortions.

An interesting political bargain that could be struck is one where changes in WPI Fuel are offset by changes in the INR/USD exchange rate. A decision to have a 10% rise in the WPI Fuel could be offset with a 10% appreciation of the rupee-dollar exchange rate. By the 10th week, the net effect is slightly negative. In addition, a rupee appreciation induces a lower price of the Indian basket of crude oil, thus helping to reduce the size of the distortion in petroleum prices. This `package deal' could thus deliver a slight reduction in prices while reducing the distortions in the economy in two key markets. It would clear the slate for the UPA in the period leading up to this last budget and last year prior to the elections.

In summary, the last two important places where the government largely sets prices are the rupee dollar exchange rate and petroleum products. The best political package would be one where distortions in both markets are simultaneously eased.

Back up to Ajay Shah's 2008 media page

Back up to Ajay Shah's home page