How to control inflation

Business Standard, 2 April 2008

Another year, another inflation crisis: India continues to pay the price for not undertaking fundamental monetary policy reform. The mess that we are in is a reflection of an inconsistent monetary policy framework. Merely raising rates will not solve the problem. The way forward lies in breaking the INR/USD peg, as was done in early 2007, and having a 10% rupee appreciation.

When inflation spikes, the single focus of the government becomes controlling inflation. This is not how mature market economies work. In all mature market economies, the task of controlling inflation - and only the task of controlling inflation - is placed with the central bank. In mature market economies, inflation crises do not arise, because the full power of monetary policy is devoted to this one task.

In their depths of anguish from dealing with this inflation crisis, the Prime Minister and the Finance Minister should channel their attention to RBI reforms. We are suffering from these problems because of the blunders of monetary policy. The possibility of such blunders needs to be eliminated by rewriting the RBI Act. The text of this Act is completely wrong in the light of the monetary economics that we know today. With a sound monetary policy framework, inflation would be stabilised, inflation crises like this would not periodically hijack the government, and distortionary short-sighted initiatives such as banning exports of certain goods would not arise.

India is in a big mess on monetary policy. The attempt that is underway consists of pegging the rupee to the dollar at a time when the dollar has dropped sharply. Dollar prices of many commodities have risen since producers do not like being short-changed with the same number of dollars. Holding Rs.40 a dollar intact, the global increase in commodity prices has been imported into India.

With increasing de facto convertibility, pegging the exchange rate to the US dollar leads to pressure to adopt the monetary policy of the US. The US has cut rates sharply. A massive interest rate differential has built up, and inspired a flourishing "dollar carry trade" involving borrowing in the US and bringing money into India. RBI has been swamped with capital flows owing to this interest rate differential.

In fighting to implement the pegged exchange rate, RBI has done market manipulation on a massive and unprecedented scale on both the spot and forward markets. The fiscal costs of this are rapidly building up. In a grim dogfight with the private sector, RBI artificially engineered a rupee depreciation, from Rs.39.12 on 1 Feb to Rs.40.46 on 17 March, in trying to break expectations of a one-way bet on the rupee. This is one of the factors which has helped to drive up inflation.

What is to be done? Raising interest rates while leaving the exchange rate regime intact is a poor answer for three reasons:

- The US 90-day rate is 1.28% and the Indian 90-day rate is 7%. With this massive interest rate differential, RBI's currency trading in January alone was over $20 billion! If this is done for a year, we will add $240 billion to reserves and start suffering an interest cost on MSS of over 2% of GDP. The bigger the interest rate differential, the bigger the pressure of capital inflows will be.

- Further, a perceptible slowdown in the world economy is visible. To a smaller extent, a slowdown is visible in India also. This is not a good time to raise rates.

- Finally, the impact of interest rates on inflation is slow and remote. Owing to policy blunders, we lack the bond-currency-derivatives nexus, the system of financial markets through which interest rate decisions by a central bank at the short-term rate are propagated into all interest rates in the economy. RBI's strategy of preventing sophisticated finance whereever it can has yielded ineffectiveness of RBI.

The answer is to be found in not tinkering with the existing policy framework but questioning it. The existing stance of monetary policy is ultimately inconsistent because it engenders inflation that Parliament will not tolerate. The key element of the policy that has to break is the rupee-dollar peg at Rs.40 per dollar.

The right combination of policy for the short-term involves:

The right combination of policy for the short-term involves:

- An appreciation to Rs.36 per dollar with

- A reduction in the short rate to 4%.

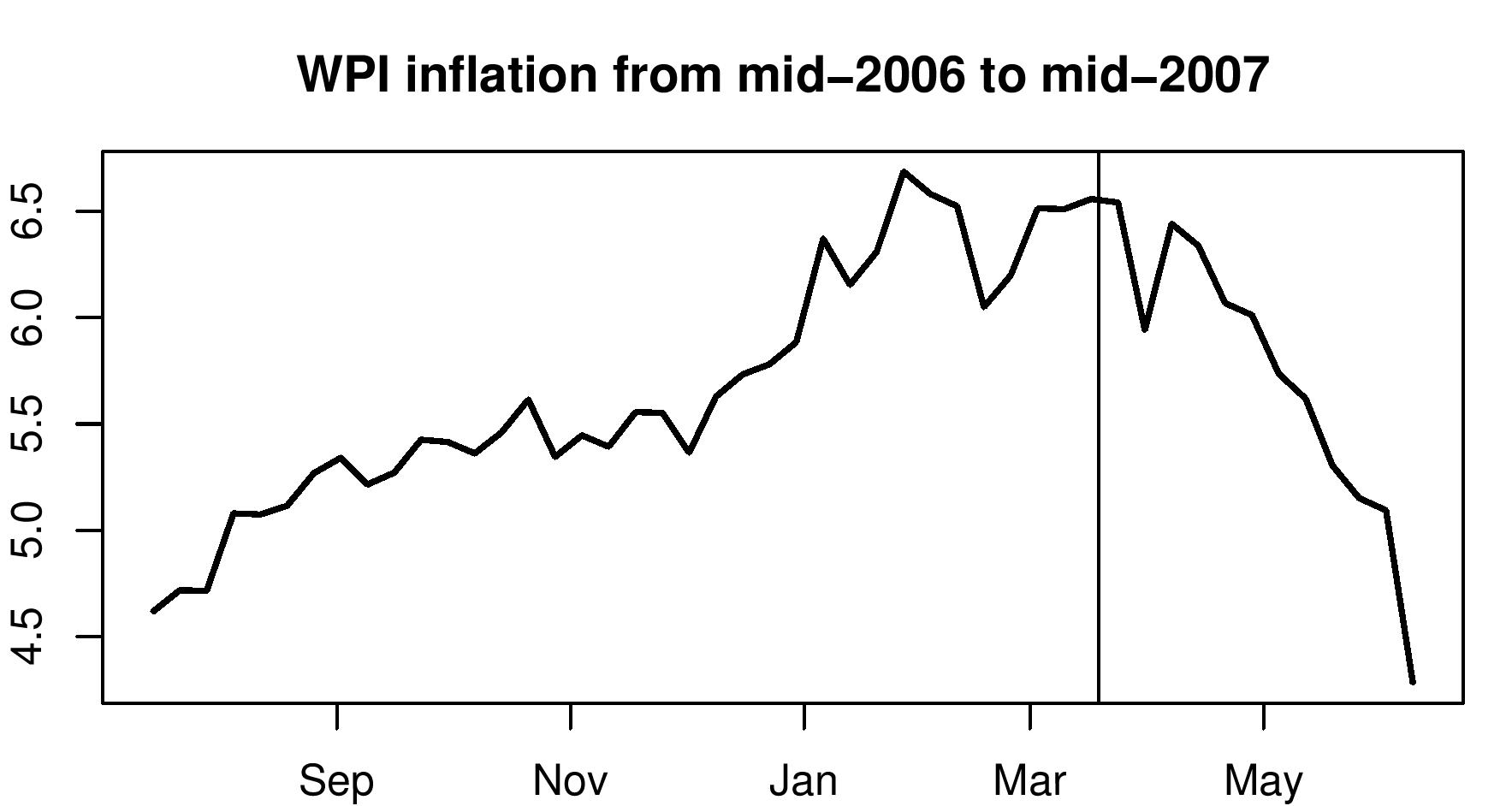

This would simultaneously hit at all the problems that we face today. A 10% rupee appreciation would yield a nice dent on inflation, as happened in March 2007 (see graph). By reducing the mispricing of the rupee, it would reduce pressure from capital flows. In addition, a 300 bps reduction in interest rates would reduce the flow of money coming into the country seeking interest rate arbitrage. To the small extent that the monetary transmission does work, this rate cut would help bolster the economy in what appears to be shaping up as a difficult time.

This combination of policies - a stronger rupee, lower rates, lower inflation - would restore the balance of a consistent monetary policy framework.

Who would gain and who would lose? The broad population would benefit from lower inflation. Exporters would suffer owing to a stronger rupee. But as we saw in 2007, the impact of the exchange rate on the WPI is sharp and visible. Exports were unaffected despite a slowing world economy: Gross earnings on the current account grew by 19% in the June quarter, 23% in the September quarter and 33% in the December quarter. Compare these against the values of 27%, 29% and 24% for the three quarters before the rupee appreciation and the world economic slowdown.

The political economy of an exchange rate appreciation is much like that of cutting customs duties. The beneficiaries of cutting customs duties are diffused and widespread. The losers are focused and engage in lobbying. Just as India found the political resources to cut customs duties despite this lobbying, the same must now be done with rupee appreciation.

Such political contests are, of course, highly distressing. The long-term answer lies in depoliticising the rupee-dollar market by focusing the central bank on inflation and getting it out of currency manipulation. An immature market economy is one where the exchange rate is stable, and where inflation and GDP growth are unstable. A mature market economy is one where inflation and GDP growth are stable, and the exchange rate is unstable. Getting there requires rewriting the RBI Act.

Back up to Ajay Shah's 2008 media page

Back up to Ajay Shah's home page