The US dollar is an unstable yardstick

Financial Express, 10 November 2008

There is a lot of focus in India on the rupee dollar rate and on RBI's foreign exchange reserves, as measured in dollars. However, the dollar is not a stable yardstick. The dollar has itself been fluctuating quite a bit. We should be careful not to read too much in changes in the rupee-dollar rate or in the level of reserves which merely reflect fluctuations of the dollar.

INR/USD

Figure 1 shows the familiar history of the rupee-dollar rate. It runs from April 2006 till the end of October 2008. This shows a depreciation of the rupee from roughly 40 to the dollar in early 2008, first to 42 and then a much sharper movement to 50 rupees a dollar. What was going on?

Figure 1 shows the familiar history of the rupee-dollar rate. It runs from April 2006 till the end of October 2008. This shows a depreciation of the rupee from roughly 40 to the dollar in early 2008, first to 42 and then a much sharper movement to 50 rupees a dollar. What was going on?

Many people think that in the global financial crisis, FII and other capital left the country, thus giving a sharp depreciation. This picture is mostly wrong.

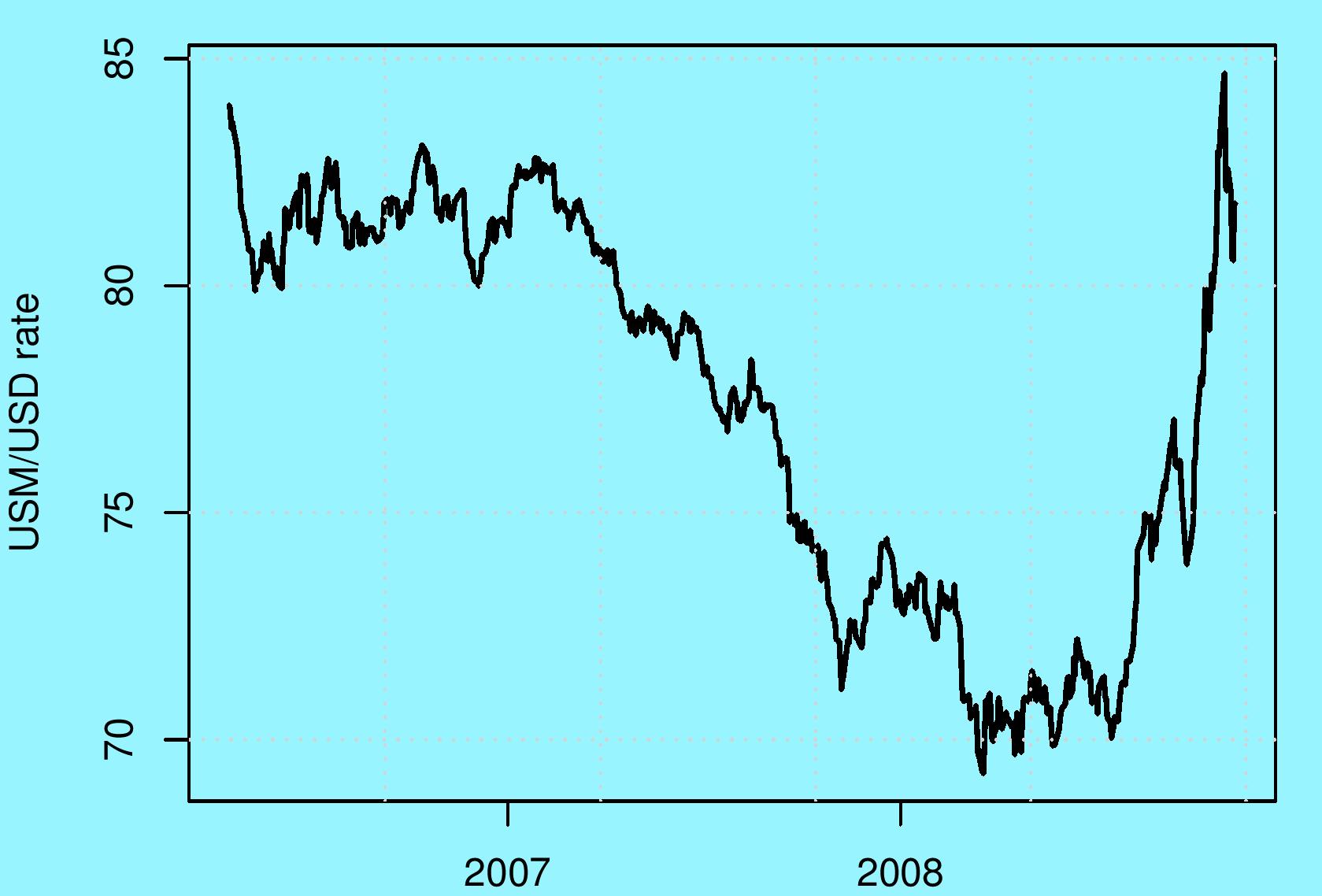

USM/USD

In order to get a better sense of what is going on, we turn to the `Major Currencies Index' maintained by the US Federal Reserve (Figure 2). This is an index of the movements of the US dollar against the major floating exchange rates of the world. This index, which is abbreviated "USM", shows a gradual dollar depreciation from the index level of 85 to 70 through 2007. In recent months, it shows a sharp appreciation of the dollar. The entire dollar depreciation of recent years has been reversed in a few weeks.

In order to get a better sense of what is going on, we turn to the `Major Currencies Index' maintained by the US Federal Reserve (Figure 2). This is an index of the movements of the US dollar against the major floating exchange rates of the world. This index, which is abbreviated "USM", shows a gradual dollar depreciation from the index level of 85 to 70 through 2007. In recent months, it shows a sharp appreciation of the dollar. The entire dollar depreciation of recent years has been reversed in a few weeks.

What has been going on is a `flight to quality'. In the global financial crisis, US and other investors are selling off many risky assets all over the world and shifting money back to US government bonds. This has given a sharp appreciation of the dollar and a decline in interest rates of US government bonds.

INR/USM

A good part of the recent rupee depreciation, then, is merely a dollar appreciation. It isn't asif conditions in India changed that much; it is the yardstick (the US dollar) that shifted. To help clarify our minds, it is useful to re-express the fluctuations of the rupee in terms of the USM. This reflects the evolution of the rupee when expressed in the major floating exchange rates of the world.

This is shown in Figure 3. This shows a rupee appreciation from 0.58 to 0.51 in 2007. The lowest point of this series is actually not the lowest point of the rupee-dollar series. By early 2008, this series shows a modest rupee depreciation back to 0.58. After that, there has been no significant movement to the recent values of 0.6. In other words, the recent rupee-dollar fluctuations are entirely about flucutations of the dollar. Expressed against the floating exchange rates of the world, the rupee has not sharply depreciated.

This is shown in Figure 3. This shows a rupee appreciation from 0.58 to 0.51 in 2007. The lowest point of this series is actually not the lowest point of the rupee-dollar series. By early 2008, this series shows a modest rupee depreciation back to 0.58. After that, there has been no significant movement to the recent values of 0.6. In other words, the recent rupee-dollar fluctuations are entirely about flucutations of the dollar. Expressed against the floating exchange rates of the world, the rupee has not sharply depreciated.

Implications for thinking about the rupee-dollar rate

When we focus excessively on the rupee-dollar rate, we are getting a wrong perception of what is going on in the currency market. The people who ask RBI to stabilise the rupee dollar rate seem to assume that the dollar is some stable store of value. It is not. It fluctuates substantially. When the dollar depreciated (i.e. when the USM declined), we tried to mechanically hang on to a fixed rupee-dollar rate. As a consequence, we were artificially inducing a rupee depreciation when this made no sense for India. Similarly, when the dollar gains strength (i.e. when the USM has gone up), if we try to mechanically hang on to some value for the rupee-dollar rate (e.g. thinking that depreciation beyond Rs.50/dollar is somehow bad), we would artifically induce a rupee appreciation mirroring the dollar appreciation, which makes no sense for India.

In our minds, we should free ourselves of this `dollar illusion' where fixity to the dollar is somehow desirable. The dollar is just one more floating exchange rate, which fluctuates based on market conditions. RBI should do monetary policy based on the needs of the Indian economy, and avoid the distortions that come from trying to manage the rupee-dollar rate. The private sector should use the currency futures market to manage fluctuations of the rupee-dollar rate.

Implications for thinking about reserves

When we see a decline in reserves (measured in dollars) we tend to assume that this was because RBI was selling dollars. But a good part of the story lies in fluctuations of the dollar. RBI holds other currencies in the reserves portfolio, such as the Euro, the Yen, the Pound, etc. The currency composition of the reserves portfolio is unfortunately not disclosed by RBI.

The size of reserves measured in billion dollars tends to be watched quite a bit. But this reflects fluctuations of the dollar against other currencies. When the dollar gains against the euro, the reserves portfolio appears to lose ground because the euro assets are now worth less. A decline in reserves is seen, but this can reflect just valuation effects.

As an example, the most recent month for which data for RBI's trading on the currency market has been disclosed is August. In this month, reserves declined by $9.8 billion dollars. But when we look at the trading data, it shows that RBI purchased $1.2 billion. The overall decline of reserves reflects a $11 billion valuation change owing to currency fluctuations. The people who focus on the change in reserves think that RBI was preventing rupee depreciation in August. But in August, RBI was trying to push for a rupee depreciation by purchasing $1.2 billion.

Many people have commented on the sharp decline of reserves (measured in dollars) in October. Data for RBI's trading will, unfortunately, only be released with a lag of several months. This leads to frenzied speculation about the difficulties that India is having in preventing depreciation of the rupee-dollar exchange rate. I would, however, hazard a guess that the bulk of the apparent decline in reserves of October 2008 was caused by the appreciation of the dollar against the other currencies in the dollar portfolio.

Back up to Ajay Shah's 2008 media page

Back up to Ajay Shah's home page