India's inflation problem

Wall Street Journal, 2 September 2008

In the mid-1990s, India achieved a major decline in inflation at the price of a highly restrictive monetary policy. After that, policy makers and the public alike thought economic policy had been put on a sound footing and that inflation greater than 5% was unlikely to materialize. These hopes have been dashed. India is in the midst of the worst inflation in over a decade, with double-digit inflation data coming out month after month. This raises serious questions about the institutional foundations of macroeconomic policy.

Part of the problem is one of measurement. In India, the commonly tracked measure of inflation is the change in the wholesale price index (WPI) over the preceding one year. This number for March, say, represents the average WPI inflation of the previous 12 months. This emphasis on the change in the price index over a year obscures the most recent changes in inflation.

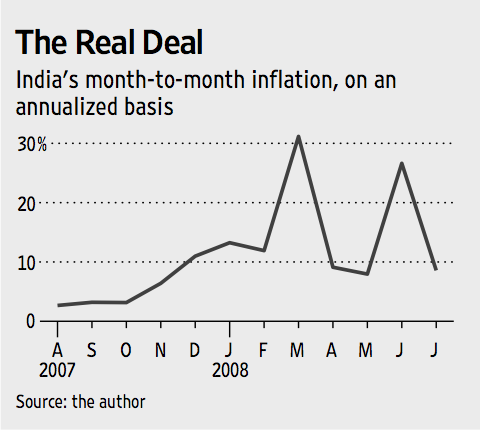

Computing seasonally adjusted month-on-month changes, as is done in most countries, reveals an even more alarming inflation picture than is commonly thought. Inflation in India jumped in December 2007, led by primary commodities and fuel. At the time, manufacturing inflation at 5.6% (on an annualized basis) was at relatively modest levels. Primary commodities continued to suffer from high inflation in January, February and March 2008. By March 2008, inflation had spread to manufacturing. In March, manufacturing inflation was 33.6% (again annualized). It has stayed at double-digit levels thereafter.

Computing seasonally adjusted month-on-month changes, as is done in most countries, reveals an even more alarming inflation picture than is commonly thought. Inflation in India jumped in December 2007, led by primary commodities and fuel. At the time, manufacturing inflation at 5.6% (on an annualized basis) was at relatively modest levels. Primary commodities continued to suffer from high inflation in January, February and March 2008. By March 2008, inflation had spread to manufacturing. In March, manufacturing inflation was 33.6% (again annualized). It has stayed at double-digit levels thereafter.

All along, the commonly cited WPI rolling averages have understated this inflation. The reading in December 2007 was 3.83%, largely reflecting subdued inflation earlier in the year. By March, it had risen to 7.48% but again, since that number included data from before the uptick started in December, it missed the significance of the trend on the ground.

This can also be a problem in the opposite direction. Even if underlying inflation now stops increasing, the WPI rolling average will show high values until the middle of 2009.

Beyond the measurement problem, there are other lurking inflationary dangers. The most worrisome is the extent to which the full increase in the price of crude oil has not been passed on to consumers owing to government intervention. But that intervention is straining the government budget and is not sustainable. When prices of petroleum products are raised, this will further accelerate inflation.

This upsurge in inflation could not have come at a worse time for the government, given the proximity of elections -- expected before next May -- and the strongly held belief among politicians that high inflation loses elections. But so far the government has merely come up with a series of distortions in physical markets, such as banning futures trading in some commodities or banning the exports of milk powder. These are ineffectual in combating the macroeconomic foundations of inflation, and merely damage investor confidence.

The two critical elements that do matter are monetary policy and the exchange rate. India does not have a properly structured monetary policy framework. The central bank is primarily focused on exchange rate pegging, and is not held accountable for price stability. As a consequence, when inflation rose sharply from December 2007 onwards, the monetary policy response was sluggish. The 90-day interest rate has risen to 8.9% in July 2008 from 7.4% in December 2007. This 150 basis-point tightening has failed to keep up with the rapid rise in inflation. It is useful to re-express the 90-day interest rate in real terms based on inflation forecasts. This rate is now negative, having dropped to minus 0.88% in July 2008, from 1.33% in December 2007a 221-basis-point easing. Monetary easing in such a difficult inflationary situation is inappropriate.

At the same time, the monetary policy transmission is weak. Various capital controls and regulatory prohibitions have prevented the bond market, the currency market and the banking system from properly passing through policy changes. As a consequence, when the central bank changes short-term interest rates, this has a limited impact upon the economy. Even if interest rates were raised today, a substantial impact on inflation in time for the coming elections would be unlikely.

Instead, exchange-rate management offers the best hope for controlling inflation in the one- to four-month time horizon. Roughly speaking, a 1% appreciation of the rupee yields a 0.2% reduction in the WPI. A strong rupee policy is thus only policy lever the government possesses, where the impact is quickly visible.

How might India adopt a strong rupee policy? The first element is shedding excessive reserves. India has build up $300 billion of reserves, well beyond what is required to assure stability. This reserves buildup entails explicit and implicit fiscal costs, and contributed to inflation because of the rupees which had to be pumped into the economy when the central bank purchased dollars.

Selling reserves would have three benefits. An exchange rate appreciation would combat inflation; the implicit and explicit fiscal costs of holding reserves would decline; and it would support the monetary tightening that helps fight inflation.

The second element of a strong rupee policy consists of easing capital controls. In 2007, a series of capital controls were introduced to discourage capital inflows and suppress the value of the rupee, thus maintaining the weak rupee policy of the time. These capital controls need to be lifted. Going beyond these, expert committees appointed by the government have emphasized the benefits from capital account liberalization, through measures such as opening up the rupee denominated bond market to foreign investors. Moving forward on these proposals would simultaneously foster financial sector development and enable an anti-inflation strong rupee policy.

Inflation is rightly an electoral issue: voters are understandably alarmed at the shrinking value of the rupee. So politicians and policy makers owe it to themselves, not to mention the public, to improve the measurement and forecasting of inflation, and then establish a sound macroeconomic policy framework to deliver low and stable inflation.

Back up to Ajay Shah's 2008 media page

Back up to Ajay Shah's home page