Interpreting recent currency movements

Financial Express, 12 October 2009

The impending dollar crisis

From 2005 onwards, the macroeconomists of the world were worried about a different crisis: the dollar crisis. The US was on a path of building up external debt at an unsustainable pace, the flip side of which was the currency distortions in China and other Asian countries. It was clear that this arrangement could not last. The most natural solution involved a large dollar depreciation.

The key question was: Would the dollar depreciate gradually, thus giving a graceful unwinding of global imbalances? There was a worrisome alternative. If foreign capital felt unsafe in the US, owing to an impending dollar depreciation, would foreigners abruptly took money out of the US, it could precipitate a crash in the price of the dollar or of US assets.

The flight to safety

All the way until early 2008, this dollar crisis was a scenario that was a big concern. From March 2008, when Bear Stearns died, and particularly after September 2008, when Lehman Brothers died, something very peculiar happened. Instead of the dollar losing ground, it appreciated sharply! International investors felt worried about financial firms and governments worldwide, and they moved money into US government bonds as the ultimate safe asset. This "flight to safety" pushed the US dollar up at a time of the worst financial crisis in the US in over 50 years.

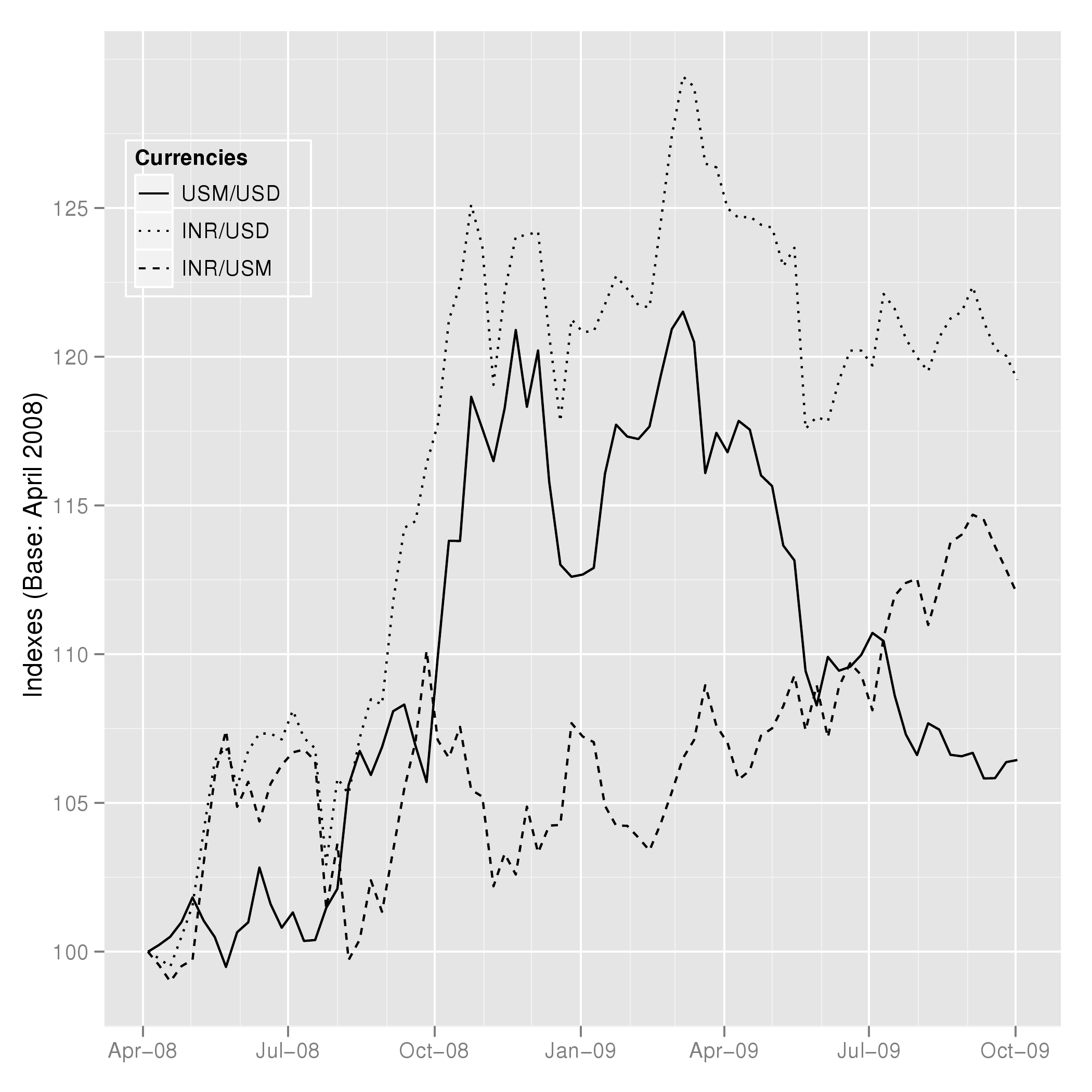

Click on the graph to see it more clearly. In the graph, the solid black line shows the time-series of the US dollar, expressed in terms of a basket of floating exchange rates. This is the US "major currencies" index, produced by the US Fed. It is abbreviated as "USM". This index went up from 100 at the start of this story to a peak of over 120, i.e. an over 20% appreciation. So far from the dollar crisis that economists were expecting, we had a remarkable and sharp dollar appreciation.

Back to the long-term dollar adjustment

By mid 2009, the worst of the financial crisis was clearly behind us. The TED Spread, which measures the extent to which big international financial firms mistrust each other, had reverted to pre-crisis values. With this, the motivation for the "flight to safety" subsided. Now, to a considerable extent, we were back to the old story of a substantial dollar depreciation being required in order to get the US current account balance down.

This decline of the dollar has begun. From a peak of over 120, the dollar index is back to 107. In other words, the US dollar has lost ground against currencies where the government does not interfere in the currency market.

What this says about the rupee

What about places like India, where the government does interfere with the market process on the currency market? As the graph shows, the dotted line for the rupee-dollar exchange rate (again, expressed as an index set to 100 at the start of this story) depreciated sharply, going up to a peak of nearly 130 or a 30% depreciation. From that peak, there has now been a a small appreciation for the rupee, where the index has come back to near 120. Overall, the rupee has had a 20% depreciation against the US dollar over this period, from April 2008 onwards.

But our fixation with the US dollar is not appropriate, since large parts of the world do not use the US dollar. Using this same "major currencies index", which reflects all the large floating exchange rates of the world, we see a different story. The dashed line shows that until February 2009, there was no large rupee depreciation, for the index of the INR/USM rate had only moved to 105 or so, for a 5% depreciation over the 10 months of crisis. From February 2009 till October 2009, there has been another 5% depreciation of the rupee.

The dollar is a fluctuating yardstick

This emphasises that a lot of the apparent rupee-dollar movement is merely a reflection of the changing fortunes of the dollar. We should not be fixated on the USD exchange rate of the rupee, for the USD is not a fixed yardstick.

When RBI tries to achieve `stability' of the rupee dollar rate, it is forcing the rupee to gyrate up and down with the fluctuations of the US dollar. In the process, whenever the US dollar loses ground, RBI is fighting appreciation, and whenever the US dollar gains ground, RBI is fighting depreciation. In other words, whenever the US dollar loses ground, interest rates in India tend to go down, and whenever the US dollar gains ground, interest rates in India tend to go up.

RBI's pursuit of stability of the rupee versus the US dollar leads to an RBI that destabilises the domestic economy. A better strategy for RBI is to think about India and only India when it comes to monetary policy.

Improve the ability of the economy to handle currency risk

The rupee-dollar rate will fluctuate, and the way to address concerns about currency risk is to permit the emergence of proper currency derivatives markets. The best currency risk management market in India today is the rupee-dollar futures market trading at NSE. However, RBI has banned most of the possibilities of this market by banning participation by FIIs and NRIs, banning futures on currencies other than the US dollar, banning options trading and banning swaps trading.

These are important mistakes in policy. India's progress towards a genuine central bank which cares about Indian business cycle conditions requires the emergence of capable currency derivatives markets. By preventing these markets from emerging, RBI hampers its own growth into a high quality central bank.

Back up to Ajay Shah's 2009 media page

Back up to Ajay Shah's home page