The bogey of exports growth

Financial Express, 1 May 2010

There is a lot of talk about rupee appreciation in recent weeks. It is claimed that rupee appreciation is bad for exports growth and that RBI must trade in the rupee-dollar market so as to force the exchange rate back to (say) Rs.50 a dollar.

Who must do export promotion?

The first issue is about the correct location for export promotion functions. In India, the Ministry of Commerce is charged with export promotion. It is not clear why RBI should carry cudgels on their behalf. If it is felt that subsidising exporters is a good idea, the right way to do this is to have an explicit on-budget subsidy. It is not healthy to have non-transparent subsidies where it is not clear what is the expenditure being borne by the government or by the economy at large, in return for what increased exports.

As an example, exports will go up if electricity is sold to exporters at subsidised prices. That does not mean that electricity policy should be distorted to suit the interests of exporters.

Can exports growth happen without exchange rate depreciation?

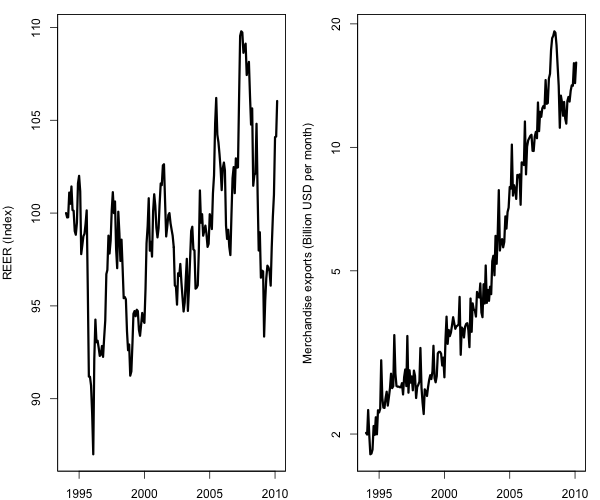

But the bigger issue is that exchange rates have much less to do with exports growth than most people seem to assume. The `real effective exchange rate' reflects the average of rupee fluctuations against all currencies, adjusted for relative inflation. Figure 1 superposes the Indian REER time series against the Indian merchandise exports time series. From 1994 onwards, the REER has fluctuated between 85 and 110. Over this period, merchandise exports have risen from $2 billion a month to $15 billion a month.

But the bigger issue is that exchange rates have much less to do with exports growth than most people seem to assume. The `real effective exchange rate' reflects the average of rupee fluctuations against all currencies, adjusted for relative inflation. Figure 1 superposes the Indian REER time series against the Indian merchandise exports time series. From 1994 onwards, the REER has fluctuated between 85 and 110. Over this period, merchandise exports have risen from $2 billion a month to $15 billion a month.

If one believed that the REER was central to export promotion, then the exports growth which has been achieved is astonishing, considering that no big REER depreciation has taken place. What is going on? The key insight is that exports growth comes from two things. First, world trade grows. When world trade does well, Indian exports do well, and vice versa. This is independent of exchange rates. Second, India has been learning to export. Gradually, firms are learning how to produce at low-cost locations in India and sell goods all over the world. That is the heart of the transformation from $2 billion a month of merchandise exports to $15 billion a month. This also has nothing to do with exchange rates.

If firms are given subsidies, they will of course enjoy taking them, but in the process less learning will take place about how to match the price and quality of the global market place. It makes sense for India to force firms to pay market prices for electricity, steel or the exchange rate.

The story of India's exports growth is even more dramatic than that portrayed in the graph, because Indian services exports grew by even more than the merchandise exports. That is a story about infrastructure (ubiquitous cheap telecom) and human capital (building up a workforce with millions of computer programmers). The exchange rate had nothing to do with India's services exports revolution.

But what about China?

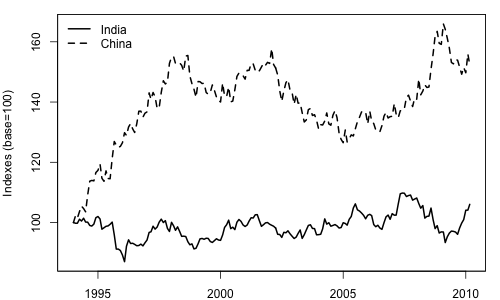

But what about China? It is argued that as long as China artificially forces down its exchange rate, India has to resort to similar tactics. Figure 2 superposes the Chinese REER against the Indian REER. In both cases, data from the Bank of International Settlements (BIS) is used - this is the best REER calculation presently available.

But what about China? It is argued that as long as China artificially forces down its exchange rate, India has to resort to similar tactics. Figure 2 superposes the Chinese REER against the Indian REER. In both cases, data from the Bank of International Settlements (BIS) is used - this is the best REER calculation presently available.

The graph shows that the Chinese real rate appreciated by 50% from 1994 till 2010. This contradicts any simplistic story about Chinese exchange rate manipulation being the essential foundation of the Chinese growth miracle. To get to Chinese-style exports growth, we have to get to Chinese-style labour law, infrastructure, education, openness to FDI, and have nearby centres of advanced capitalism like Hong Kong and Taiwan. The exchange rate is a sideshow when compared with these bigger issues.

Does the government control REER?

Why has the Chinese real rate appreciated as it has? The key lies in understanding that a country actually does not control its real effective exchange rate. Suppose RBI tries to do market manipulation on the rupee-dollar market. They would do this by purchasing dollars and paying for this in rupees, trying to drive up the dollar. When this is done, rupees get released into the system. These ultimately result in inflation. When inflation comes along, as it inevitably will, the REER goes up.

In the jargon of economists, nominal instruments cannot control real outcomes. In the end, we cannot prevent REER appreciation when India becomes more productive. We can just choose whether (in addition to REER appreciation) we want it accompanied by market manipulation by the central bank, and the attendant inflationary pressure.

Fallacies of this field

It is hence useful to question many of the statements which are being widely claimed.

Exports growth is about the deeper problems of India, such as infrastructure or education or labour law or the GST. It is also about world trade growth. It has very little to do with the REER.

And even if it did, government has little influence over the REER. Even if RBI tries to do market manipulation on the rupee-dollar market, it cannot stave off REER changes since nominal instruments cannot modify real outcomes.

If government wanted to subsidise exporters, the right place to do this is to run export subsidy programs in the Ministry of Commerce. The wisdom of doing this is questionable - India gains GDP growth from export orientation only when exporters compete in the world economy and match world price at world quality. If feeble exporters show fake exports propped up by subsidies such as tax exemptions or free electricity or a manipulated exchange rate, we get the pointless combination of subsidising foreign consumers coupled with a lack of productivity growth.

Back up to Ajay Shah's 2010 media page

Back up to Ajay Shah's home page