Areas of weakness in the thinking of financial traders

Business Standard, 8 February 2016

The stock market processes information well in some respects. It's very hard to use stock prices to forecast stock prices. What about the forecasting of fundamentals? The stock market seems to do relatively well in "micro-forecasting": differentiating one company from another. The stock market does not seem to do well at "macro-forecasting": in understanding the overall trajectory of Indian earnings growth.

Financial markets are information processing engines. A large number of speculators look at the world, make forecasts about the future, and place bets. They are not armchair forecasters, they put their money where their mouth is. It is interesting to ask: How well does the stock market fare, in consuming information and producing informative prices?

Is price data utilised efficiently?

Let's start at the forecastability of prices. In a well functioning market, all news is impounded into the price, and tomorrow's fluctuation depends on tomorrow's news. Some people think that randomness of price movements proves that markets work badly. However, as tomorrow's news is unpredictable, tomorrow's fluctuation should be unpredictable. Unpredictability of movement of prices is the hallmark of a market that is working well.

The market does well in this respect. It is very hard to forecast prices by using price data. There are chinks in the armour of market efficiency, but they are small deviations from the ideal state. Only by going into high frequency data such as one minute or one second do we stand a chance, of using price data to forecast prices. These small edges are being competed away, as more securities firms gain mastery of algorithmic and high frequency trading.

Prices as forecasts: Micro-forecasting

What about fundamentals? The market price measures the aggregative opinion of all the speculators. If they are doing a good job of understanding the world, they should have forecasting power. Let's first think about "micro-forecasting", or thinking about one security at a time.

If there are two similar firms, and one is awarded a P/E ratio of 10 while another is awarded a P/E ratio of 20, is there merit here? In 1999, we discovered that the answer is Yes. The P/E ratio turns out to be reasonably well correlated with earnings growth in the coming five years. By and large, the stock market does seem to do well in looking at one company at a time and making calls about future earnings growth. Through this, the market is giving out incentives to managers to do the things that will foster future earnings growth: the firms which establish high prospects are rewarded with higher valuations.

Prices as forecasts: Macro-forecasting

The other dimension of linking prices to reality is "macro-forecasting", or thinking about the overall Indian economy. Let's focus on the P/E ratio of the CMIE Cospi index, which is a broad market index that covers all listed companies that achieve a certain (low) threshold of market liquidity. From 1999 till today, the number of firms in this index have ranged between 900 and 2800. If the stock market were a good macro forecaster, periods with a high Cospi P/E ratio would precede a big earnings expansion, and vice versa. The data does not show a strong pattern of this nature.

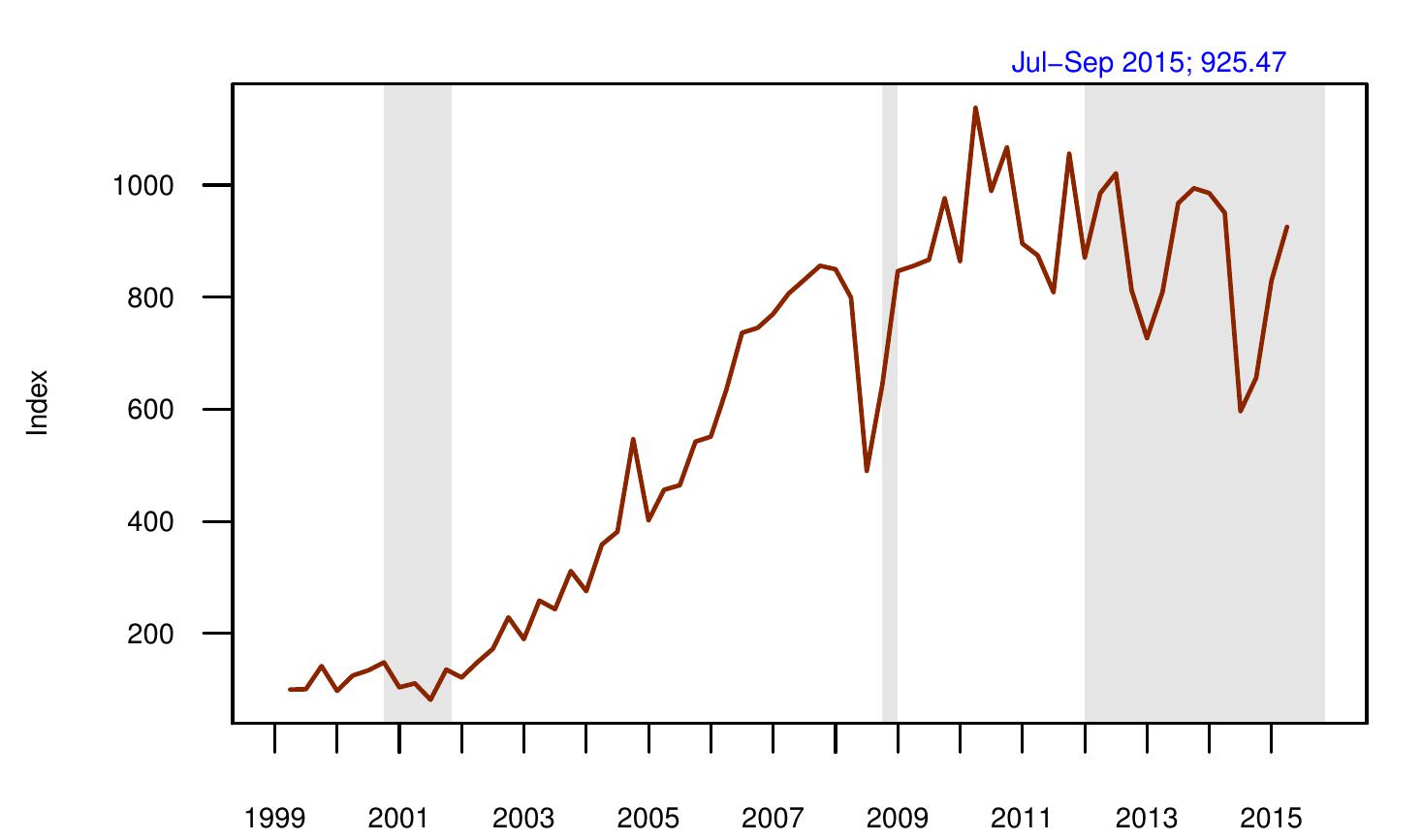

Figure 1: Index of net profits of all non-financial listed firms. Source: CMIE database, processed by the author. Shaded bars are recessions.

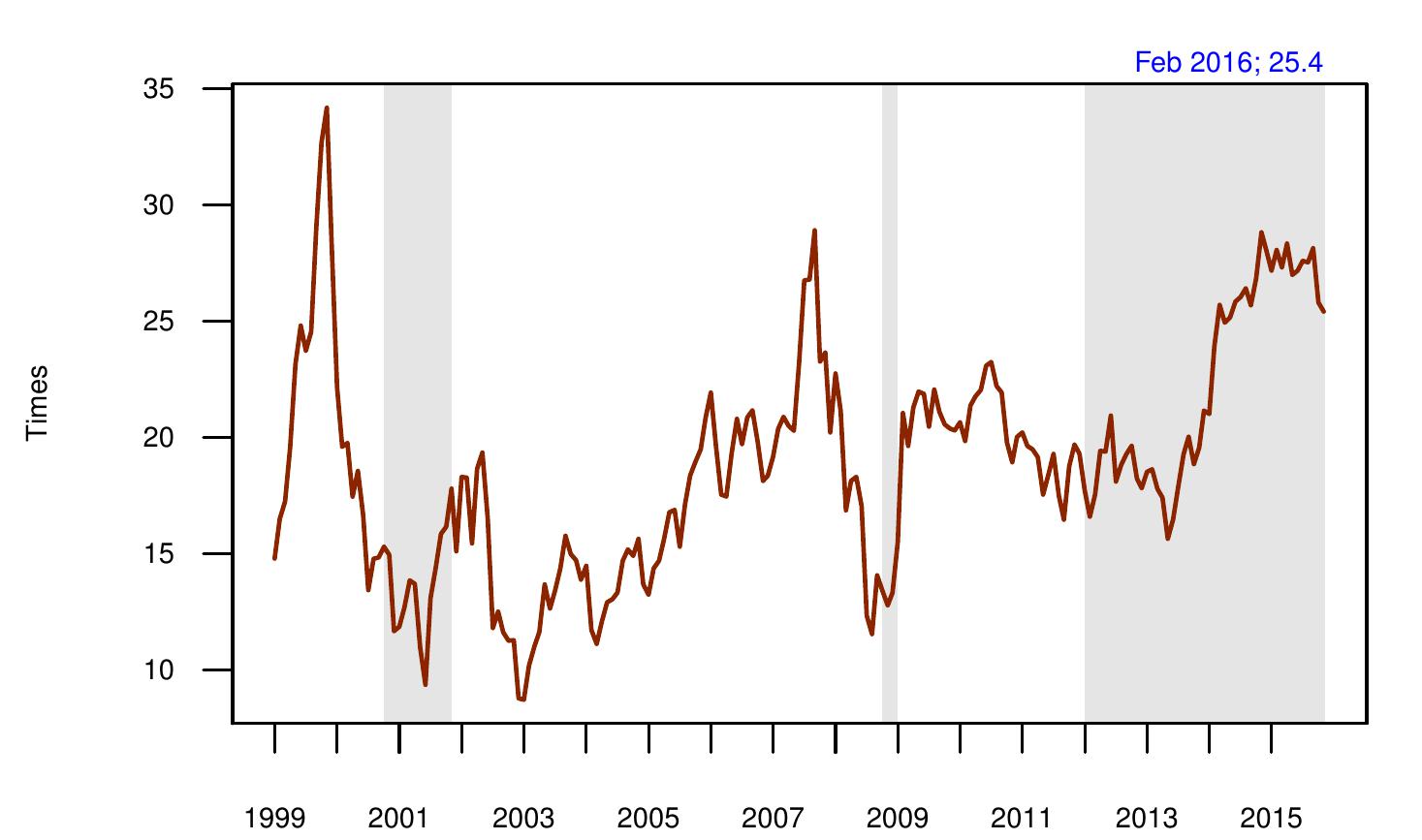

Figure 2: P/E ratio of the CMIE Cospi index. Shaded bars are recessions.

The market-wide P/E was above 30 in 1999, but earnings were flat till 2002. The biggest single expansion of earnings in India's history took place from 2002 to 2008 where the net profit went up by 9 times. The P/E ratio of the overall market didn't anticipate this. During the earnings expansion from 2002 to 2009, the market appears to have slowly caught up with the remarkable developments. As late as 2003, the P/E ratio was below 10, showing a lack of appreciation for what had already begun. The P/E ratio gradually went up after the earnings growth was demonstrated. It peaked at near 30 at the end of this phase of earnings expansion. The market failed to see that things were going to get difficult from here on.

With the benefit of hindsight, we know that there was negligible earnings growth from 2008 till 2015. A period of 9-fold earnings expansion from 2002 till 2008 was followed by a period of flat earnings from 2008 till 2015. The market wide P/E ratio failed to see that. In 2010 the market felt that the Lehman crisis was over and we are back to normal. The market was wrong. From early 2014, the market-wide P/E ratio doubled from 15 to 30. So far this forecast has not proved correct.

Implications

The picture thus seems to be in three parts: the market is doing well on utilising price information, with a frontier in high frequency trading which is pushing the zone of non-forecastability of prices to ever smaller time horizons. The market is doing relatively well in security analysis. A lot of people are studying individual companies. By and large, there is good sense in the differential valuations being awarded to firms. Managers who build for future growth are being rewarded by the market. However, by and large, the market is failing at macro forecasting.

Market-wide earnings growth is arguably the dominant phenomenon which shapes the performance of portfolios. E.g. the 9-fold increase in earnings from 2002 to 2008 was the dominant story of portfolio performance of that period. The market does not seem to be understanding this.

We can conjecture two kinds of expanations. Perhaps macro-forecasting in India is too hard. Indian macroeconomic data is a shabby mess, and very little is known about Indian macroeconomics. While people may try to divine the future, this is a hopeless task.

Alternatively, perhaps macro forecasting is under-resourced. The macro thinking that's being done by financial firms today is overly simplistic. What's needed is paying less attention to the official government statistics and press releases, developing new ways to measure the economy, and forming a view about the future. On the margin, the information processing in finance should favour this.

Back up to Ajay Shah's 2016 media page

Back up to Ajay Shah's home page