Combating inflation

Business Standard, 6 June 2007

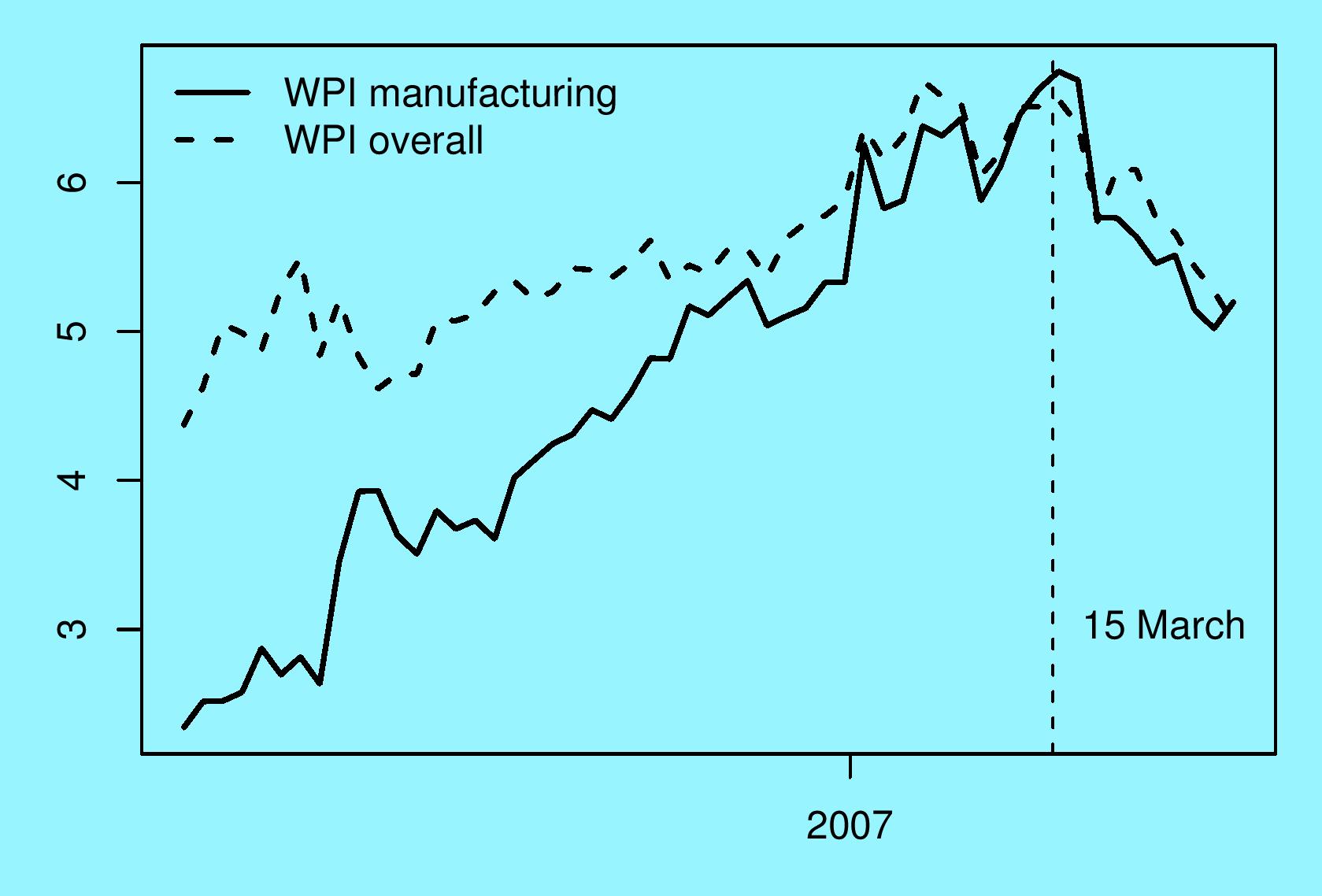

The graph shows weekly data for year-on-year inflation for the overall WPI and for WPI manufacturing. When WPI inflation accelerated sharply, the government unleashed a slew of policy initiatives inspired by 1970s economics. It attacked hoarders, speculators and profiteers. Futures trading was banned in some cases; exports were banned in others. As the graph shows, this litany of bad economics achieved absolutely nothing in terms of denting inflation.

The graph shows weekly data for year-on-year inflation for the overall WPI and for WPI manufacturing. When WPI inflation accelerated sharply, the government unleashed a slew of policy initiatives inspired by 1970s economics. It attacked hoarders, speculators and profiteers. Futures trading was banned in some cases; exports were banned in others. As the graph shows, this litany of bad economics achieved absolutely nothing in terms of denting inflation.

For many months, RBI staff delivered stirring speeches about inflation control. Under the shroud of non-transparency, what RBI was actually doing was focusing on manipulation of the currency market. While RBI was claiming to be concerned about inflation, they were actually fueling it.

RBI does not release daily data about its currency trading. However, an examination of the rupee-dollar exchange rate shows that the old exchange rate regime broke on 15 March. A rupee appreciation of roughly 10% took place after that. This was a big change in policy. The government had changed gears, refocusing monetary policy away from the currency to domestic inflation.

Did it work? The inflation experience lines up rather well with the date on which the currency policy changed. As the graph shows, WPI inflation peaked at the date of regime change, and dropped dramatically after that. The WPI release of 17 March was the peak - with overall inflation of 6.56% and manufacturing inflation of 6.75%. The latest data, dated 19 May, shows an improvement of 1.5 percentage points for both when compared with the peak.

This is an important victory over inflation. It helps to break the inflationary expectations which were starting to set in, with a wage-price spiral.

Why did a change in the currency regime generate a 150 bps drop in WPI inflation in two months?

- The first thing going on is the footprint of import parity pricing in the economy. The domestic price of steel - even the steel produced by SAIL - is the world price of steel multiplied by the exchange rate. For an increasing list of products, firms in India are invoicing - every day - by taking world prices and multiplying by the prevailing exchange rate. Where there is import parity pricing, the impact of rupee appreciation on prices is immediate.

- After this, there are downstream effects - where cheaper raw materials (e.g. cheaper steel) propagate into the prices which are not governed by import parity pricing (e.g. cars) - with a lag. A statistical analysis shows that the full effect of an impulse of rupee appreciation upon the overall WPI plays out in roughly 4-8 weeks.

- Another impact works through a shift in aggregate supply/demand conditions in the economy. INR appreciation reduces export demand which helps reduce overall prices.

- Another factor is monetary policy. As Vivek Moorthy has emphasised, RBI's withdrawal from the currency market made possible a monetary policy which was not compromised. However, monetary tightening plays out over a much longer timescale.

- The overall WPI is made up of three components: manufacturing, primary goods and fuel. Fuel prices were not changed by the government. The drop in both WPI manufacturing and in the overall WPI, that is depicted in the graph, was possible because WPI primary also fell nicely.

This drop in WPI primary comes as a surprise. Traditionally, in India, it is felt that primary prices are primarily about politics and not economics. However, while government is important for the price of wheat or rice, it does not directly interfere in a large set of agricultural commodities of growing importance, such as vegetables, fruit, meat, milk, etc. These markets are part of the normal rules of a market economy: prices are formed by a very large number of buyers and a very large number of sellers. Prices of many agricultural commodities are influenced if not determined by import parity pricing. When interest rates go up, people have less money to spend, which leads to lower purchase of milk products and thus lower milk prices.

What does the future hold? My calculations suggest that the impact of rupee appreciation to Rs.40.5 upon inflation have largely played out. Further developments on inflation now depend on monetary policy.

While it seems that a good victory over inflation has been scored, there are three key hurdles to cross:

- The WPI is a poor measure of inflation. The best inflation measure in India is the CPI-IW. This data comes out with a long lag. Policy makers need to keenly watch CPI-IW and keep score by it.

- While a gain of 1.5 percentage points is nice, what India needs to shoot for is an inflation target of 3%. Sound macro policy involves inflation which is "low enough to not matter". Anything above 3% injects inflation considerations into the everyday decisions of firms and households. Monetary policy needs to keep its eye on the ball and ensure that CPI-IW inflation gets back to 3%.

- The third hurdle is monetary policy. Given the non-transparency of RBI, it is not possible to tell what monetary policy is doing. However, there is surely something amiss when interest rates on the call money market are at zero percent. A negative real rate is surely not a monetary policy stance that is consistent with obtaining a deceleration of inflation. It could be that RBI is back to its old game of manipulating the currency market. Policy makers need to ensure that RBI does not take its eye off the inflation ball.

The UPA needs to get inflation back to 3% by late 2008 in time for the next general elections. This requires a restrictive monetary policy - short-term real interest rates have to be atleast 3 percent in order to reduce inflation. Going beyond petty political gains, when monetary policy does not deliver the goods of low and stable inflation, it has serious consequences. Fluctuations of inflation hinder the decision making of private firms. Inflation volatility brings out the worst in Indian economic policy making such as banning the exports of milk or futures trading on wheat. It destabilises capital flows and the financial sector, increases GDP growth volatility, and reduces GDP growth. Reform of the institutional framework of monetary policy is required, to ensure that instability of inflation - from 3% in 2004 to 7.5% and then hopefully back to 3% by 2008 - does not recur.

Back up to Ajay Shah's 2007 media page

Back up to Ajay Shah's home page