Where we stand on the currency futures market

Financial Express, 13 October 2008

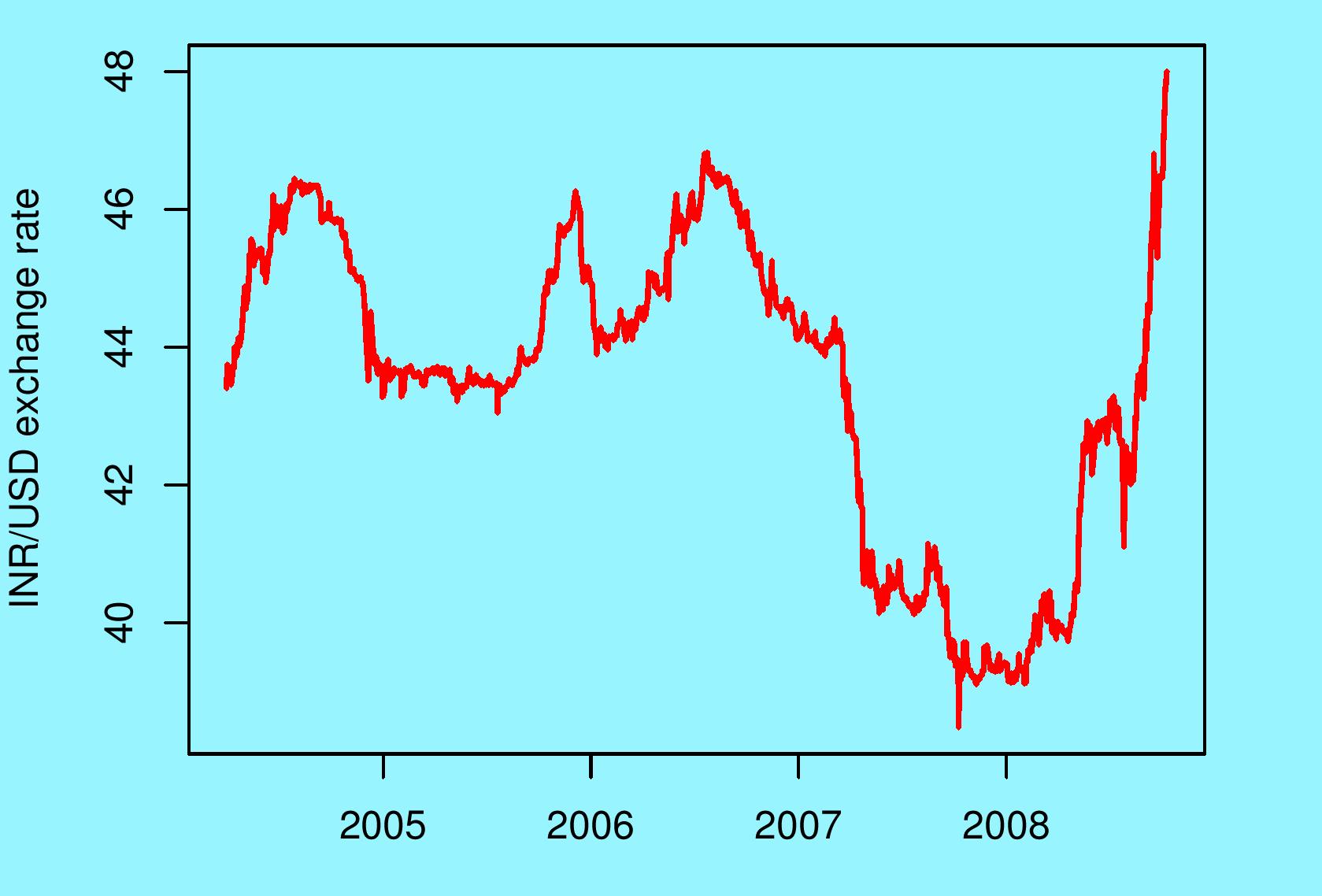

The rupee-dollar exchange rate has fluctuated substantially. Over the last year, RBI appears to have been permitting a market determined exchange rate to a greater extent, as opposed to the efforts that used to take place earlier to prevent the market from determining the exchange rate.

The rupee-dollar exchange rate has fluctuated substantially. Over the last year, RBI appears to have been permitting a market determined exchange rate to a greater extent, as opposed to the efforts that used to take place earlier to prevent the market from determining the exchange rate.

A lot of households and firms are thus presented with currency risk, or the losses that they could suffer if adverse currency movements took place. Some people could lose if the rupee depreciates (e.g. importers) while others could lose if the rupee appreciates (e.g. exporters). All of them require a healthy currency derivatives market on which hedging, speculation and arbitrage involving a variety of exchange rates can be done.

In the aftermath of the Percy Mistry and Raghuram Rajan reports, exchange-traded currency derivatives trading has begun in India. This is one of the most important milestones in India's financial system development. At present, the biggest financial product in India is derivatives on the Nifty index. These are futures and options which are cash-settled based on the official value of Nifty. In identical fashion, futures on the rupee-dollar rate are cash-settled to the official rupee-dollar exchange rate. One contract on this market pertains to $1000. As an example, an order for 1000 contracts of the INR/USD futures is an order for $1 million.

The key advantage of the currency futures market is transparency and competition. The NSE screen is fully transparent. There can be no cheating on the price. And, all NSE members offer the service of taking orders; their competition drives down the intermediation charges. NSE's clearing corporation absorbs the credit risk of this market: if any one securities firm goes bankrupt, the clearing corporation ensures that no counterparty is affected. These design features make the currency futures market a safe place to transact.

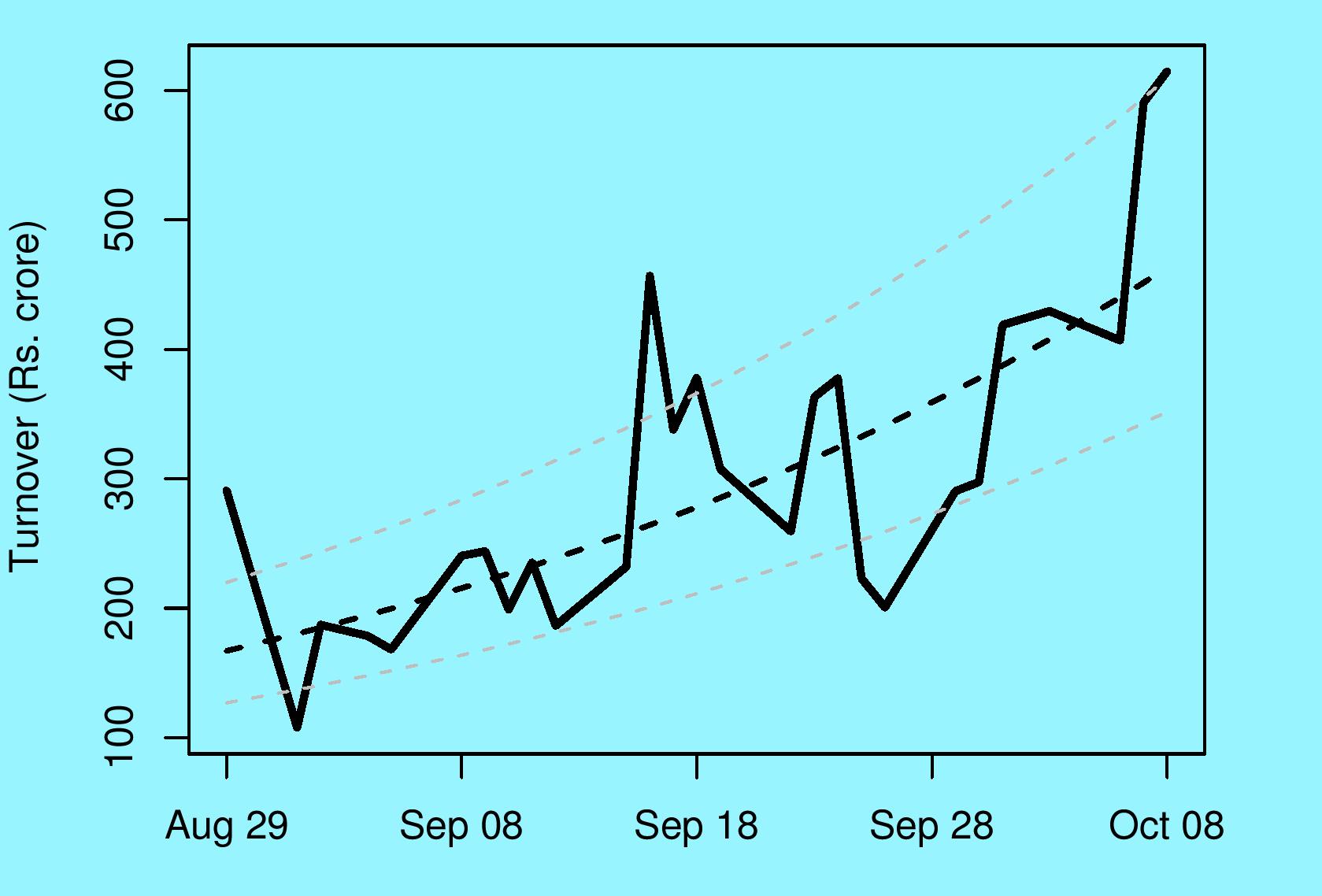

In this time of unprecedented uncertainty about the currency, trading volume has risen rapidly after the permission was given. The figure shows the time-series of trading volume on the dollar-rupee futures at NSE. In the early days, it was at roughly Rs.200 crore a day. This has gone up to roughly Rs.600 crore a day over a period of roughly 1.5 months. If the key policy constraints are removed, there is a good chance that currency derivatives would be bigger than equity derivatives.

In this time of unprecedented uncertainty about the currency, trading volume has risen rapidly after the permission was given. The figure shows the time-series of trading volume on the dollar-rupee futures at NSE. In the early days, it was at roughly Rs.200 crore a day. This has gone up to roughly Rs.600 crore a day over a period of roughly 1.5 months. If the key policy constraints are removed, there is a good chance that currency derivatives would be bigger than equity derivatives.

The bid-offer spread of the market has proved to be usually one paisa or less. Suppose the ideal price of a product is Rs.100, and a buyer of a certain quantity ends up paying Rs.101 when a market order is placed. In this case, we say that there was an `impact cost' of 1%. On the currency futures market on October 7, for a transaction size of $50,000, the impact cost was typically 0.02%. For a transaction size of $500,000, the impact cost is typically 0.05%.

These impact cost calculations are pessimistic in that they assume that a single order is placed into the market to buy at whatever price is available on the market. In my experience, I have seen that whenever an order for $500,000 or $1,000,000 is placed somewhere between the best buy and best sell prices, within a minute, the entire order is matched. There is a lot more liquidity in the eyeballs watching the screens as compared with the orders visible on the screen.

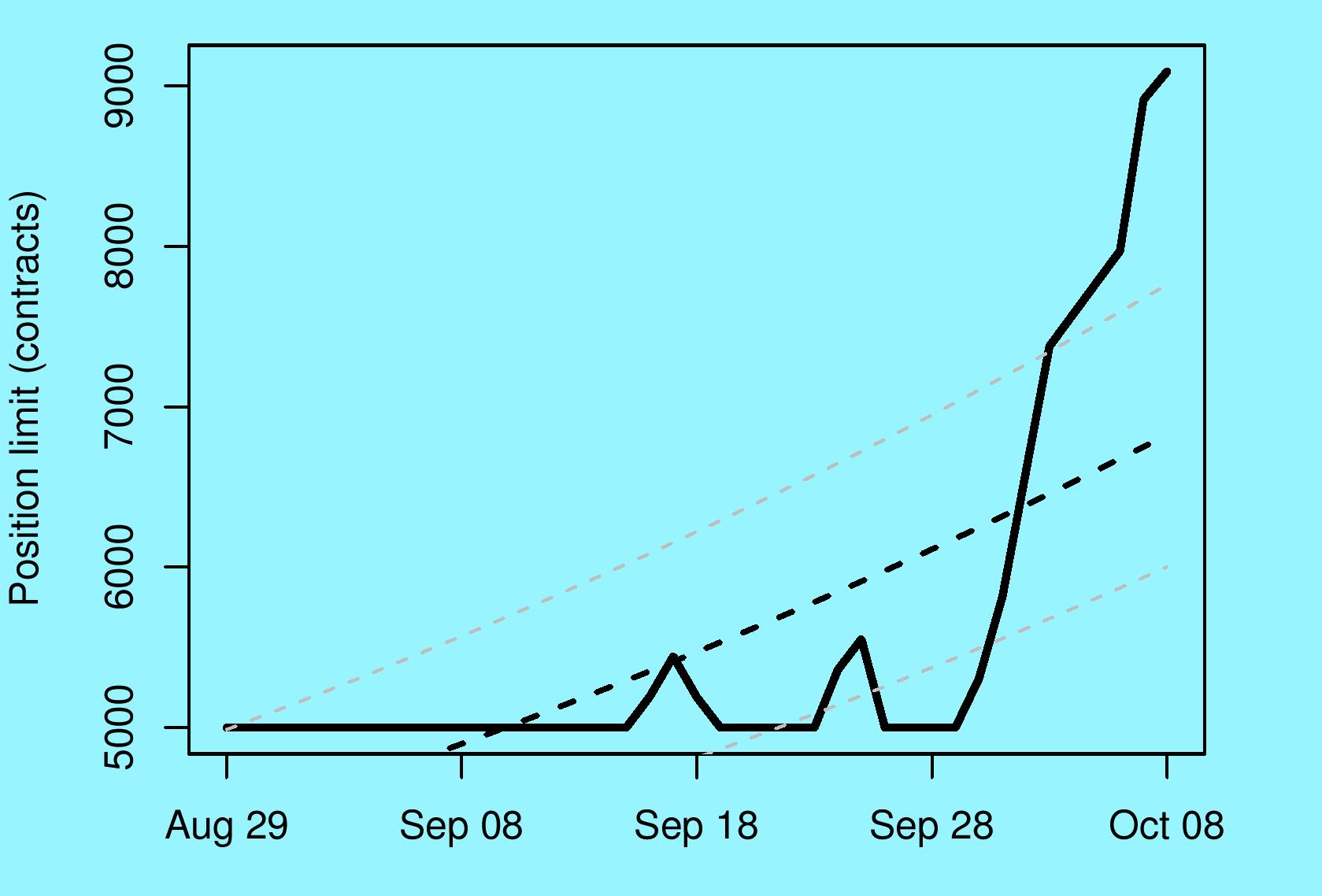

RBI has placed numerous restrictions against this market. The only currency pair that can be traded is the rupee-dollar rate. The only product that can be traded is futures. FIIs and NRIs are prohibited. The most damaging restriction is that the position of any one player is limited to 6% of the open interest of the market (or $5 million, in case the open interest is too small). The figure shows how this position limit has grown as a consequence of the growth of the open interest of the market. While in the early days of the market, positions were limited to $5 million or roughly Rs.25 crore, the limit has now climbed to $9 million or roughly Rs.45 crore.

RBI has placed numerous restrictions against this market. The only currency pair that can be traded is the rupee-dollar rate. The only product that can be traded is futures. FIIs and NRIs are prohibited. The most damaging restriction is that the position of any one player is limited to 6% of the open interest of the market (or $5 million, in case the open interest is too small). The figure shows how this position limit has grown as a consequence of the growth of the open interest of the market. While in the early days of the market, positions were limited to $5 million or roughly Rs.25 crore, the limit has now climbed to $9 million or roughly Rs.45 crore.

While this is not a useful number for the biggest corporations, there is a very large number of small and medium enterprises who face currency risk of this magnitude. The issues of high transparency and low intermediation costs are particularly important for these kinds of users, who are otherwise treated badly by financial firms in their currency hedging requirements.

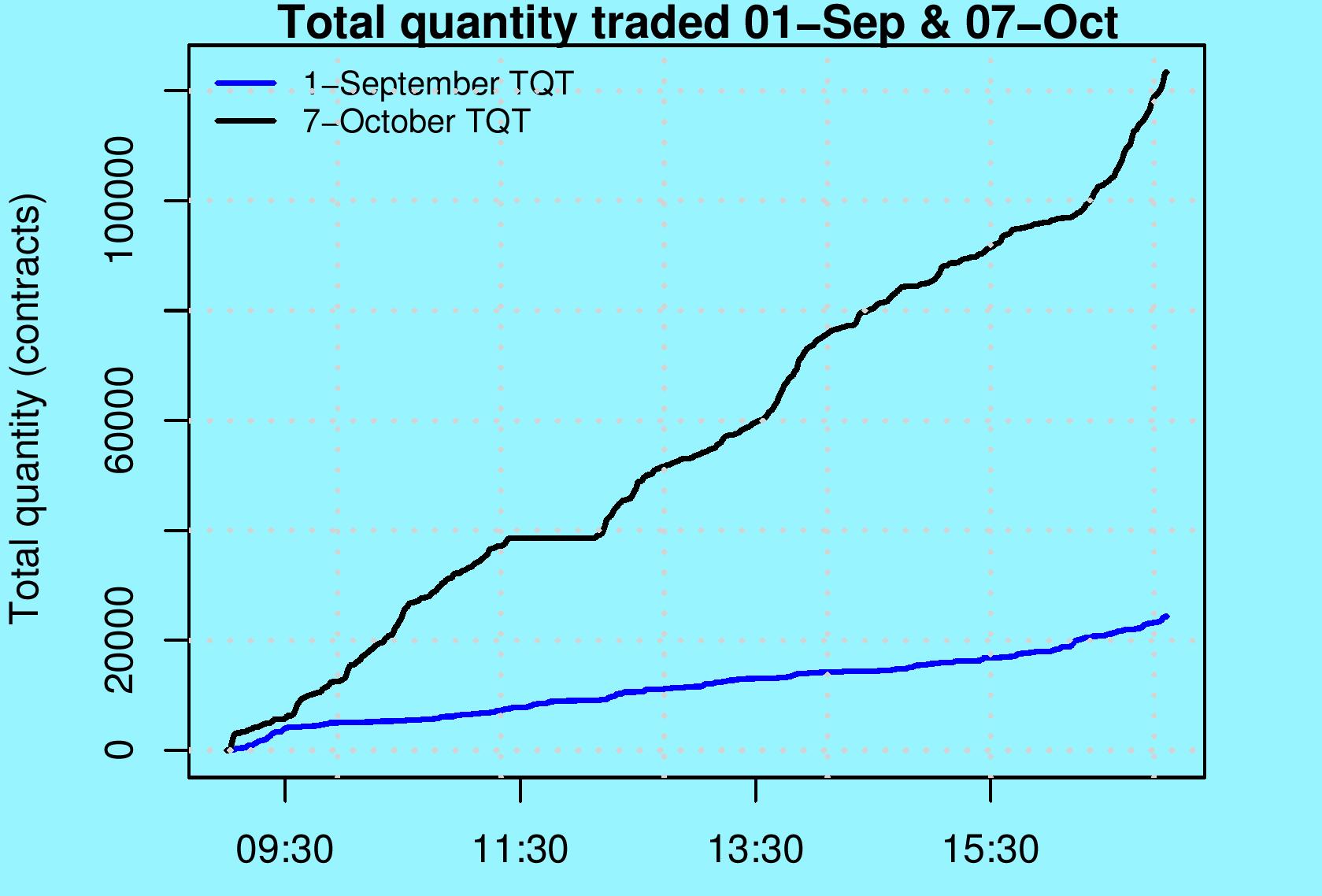

In early september, the NSE order book used to contain roughly $2 million of orders in the top 20 prices. In early October, this number has risen to roughly $5 million. This conveys the growth of the market. The figure shows the growth of total quantity traded over the trading day, comparing 1 September and 7 October. This shows the dramatic increase in market activity over the month of September. On 1 September, at 3:30 PM, 20,000 contracts or $20 million had been traded. By 7 October, this much trading was done by 10:15 AM.

In early september, the NSE order book used to contain roughly $2 million of orders in the top 20 prices. In early October, this number has risen to roughly $5 million. This conveys the growth of the market. The figure shows the growth of total quantity traded over the trading day, comparing 1 September and 7 October. This shows the dramatic increase in market activity over the month of September. On 1 September, at 3:30 PM, 20,000 contracts or $20 million had been traded. By 7 October, this much trading was done by 10:15 AM.

In summary, the rise of currency futures is a major development in Indian finance. This is a key building block of the Bond-Currency-Derivatives Nexus, and the breaking down of the silo system, that was proposed by the Percy Mistry and Raghuram Rajan committees. In a time of enhanced currency volatility, this market will play an important role in helping households and firms cope with currency risk.

Back up to Ajay Shah's 2008 media page

Back up to Ajay Shah's home page