Happy birthday, Inflation Targeting

Business Standard, 24 February 2020

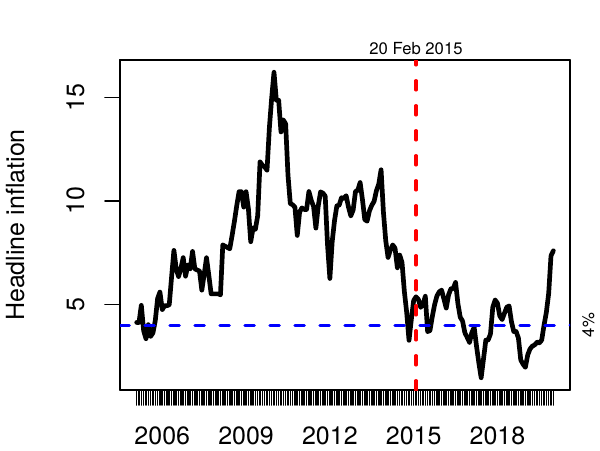

The story of inflation targeting in India starts at November 2005, when CPI inflation jumped to 5.3%. As the graph shows, the decade leading up to inflation targeting was one long inflation crisis. This raised new questions about monetary policy strategy, and also about the principal-agent relationship between the Parliament / Ministry of Finance on one hand and the RBI on the other.

The economy had become more integrated into the world, and greater financial deepening had come about. As a consequence, the intuition of monetary policy in a closed economy had stopped working. That old intuition is what got us into this prolonged inflation crisis. There was a need for new knowledge in open economy macroeconomics.

This long inflation crisis also raised questions about the nature of RBI as an agent. Every government agency must have a clear objective. In return for wielding coercive power (or spending public money), it must deliver on a measurable outcome. The authority to print money comes to RBI through Parliamentary law. The 1934 Act, through which RBI had come into existence, had correctly positioned that design of RBI as a "temporary" measure. It was time to find a better and more permanent arrangement. When the Parliament gives RBI the power to print money, what does RBI give the Parliament in return, in the form of accountability?

Inflation crises are harmful. In India, inflation harms the poor the most. Through this, inflation is directly salient for politicians. No politician wants to go into elections holding a poor performance on inflation.

It is the job of monetary policy to deliver low and stable inflation. When RBI fails, there is tremendous political pressure to find other tools -- any tools! -- to bring down inflation. When I joined the Ministry of Finance in 2001, Bimal Jalan gave me great advice, and one of the things that he talked about was inflation. He said that when inflation is under control, you can think about economic policy, but when inflation reaches 8 per cent, you have to stop doing everything else, and only do inflation control.

Inflation crises thus degenerate into a litany of woe, with real sector interventions like banning and unbanning exports or imports, changing duties, etc. These interventions damage the working of the market economy. When RBI fails to deliver on low and stable inflation, we slip into muscular real sector interventions, which damage the foundations of the market economy. It is much better to not have an inflation crisis in the first place.

None of these questions are new, on the international scale. All countries face these same problems. How to hold a central bank accountable? How to achieve low and stable inflation? The dominant solution that has come about, worldwide, is to create a formal system where the central bank is held accountable to deliver on an inflation target.

This is what led to the `Monetary Policy Framework Agreement', on 20 February 2015, which setup the inflation targeting framework as a contract between MOF and RBI. One year later, the RBI Act was amended, and inflation targeting was placed inside the RBI Act as the objective of RBI. It is fitting that, alongside this amendment, the text from 1934 which portrayed RBI as a temporary measure was removed. For the first time, RBI had clarity of purpose, it was no longer a temporary arrangement.

How well has the new framework worked? Better than anyone had expected! Practical people think that inflation is about crops and rain. It is a very intellectual concept, to think that how we wield fiat money is the dominant influence upon inflation in the long run. In fact, the high intellectual concept worked out: while crops and rain have fluctuated as always, inflation came under control once the Monetary Policy Framework Agreement was signed.

There was one blip in the data: point-on-point (seasonally adjusted) inflation in December 2019 was 21.3% annualised. This will have an impact on the year-on-year inflation for 12 months. But this is not a deeper inflation problem: point-on-point (seasonally adjusted) inflation in January 2020 was back to 3.04% annualised. Crops and rain generate volatility but not systematic inflation.

In the main, this was a historic reform, the first construction of an institutional arrangement for fiat money in India. There are three weak links which now need to be addressed. The first problem is about the composition of the Monetary Policy Committee, that gives control to one person, the RBI Governor. The second problem is the tension between the monetary policy objective and the debt management objective: the function of public debt management needs to move out of the RBI. The third problem is the weak monetary policy transmission: reforms of the bond market, of banking and of capital controls are required to make the monetary policy decisions of the MPC more potent.

There is talk about a provision in the law, which requires a review of the inflation targeting framework after five years, i.e. in February 2021. A glance at the law shows that there is no scheduled review of the inflation targeting framework in five years. What is envisaged is a review of the target: to evaluate whether there is a case for changing the target from 4% year-on-year inflation to something else. Once the three problems enumerated above are solved, it would make sense to further go down to a 2% target.

There are many calls for loose monetary policy and loose fiscal policy in order to combat the slowdown in the economy. A little institutional memory will help greatly. The one thing that we do not require, in addition to the problems of economic policy today, is an inflation crisis or a fiscal crisis. The most that monetary policy can do is to create an atmosphere of stability and predictability. This makes it possible for households and firms to look deep into the future and make plans in a state of confidence. Weakening the institutional arrangements of fiat money will not encourage private investment.

Back up to Ajay Shah's 2020 media page

Back up to Ajay Shah's home page