Indian currency manipulation

Business Standard, 16 April 2018

The US Treasury has recently placed India on a watchlist on the issue of currency manipulation. Two of their three tests make no sense, but there are grounds for concern about the third one. India had made great strides on achieving a market determined exchange rate with Dr. Reddy's decisions in 2003 and 2007, and then Dr. Subbarao's decision to stay off currency trading. In an important reversal of reforms, we have gone back to pre-2007 conditions. This is inconsistent with the RBI's statutory objective -- inflation targeting -- and puts the country in a more vulnerable place.

The three tests

The April 2018 release of the document Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States, by the US Treasury, names India for the first time. This document flows from the obligations placed upon the US Treasury, by legislation in 1988 and then 2015, to watch for currency manipulation worldwide. Their approach relies on three tests.

The first test -- a large bilateral trade surplus with the US -- is analytically wrong. The economic strategy of a country should be judged in its entirety. It is always possible and reasonable for India to run a large deficit with Saudi Arabia and a large surplus with the US.

The second test -- a large current account surplus -- is also analytically wrong. The current account surplus is the gap between investment and savings. When there is gloom in India, and investment declines, this will show up as a current account surplus. Countries should move investment through time, as conditions change, and this will result in large deficits (when optimism is high) and vice versa. The international capital market should move capital from countries with surplus savings to countries with buoyant investment. The healthy state of the world is one where some countries have large current account deficits and others have large current account surpluses.

The third test is the interesting one. The US treasury looks for large scale currency trading and persistent one-sided currency intervention. India seems to have breached this criterion.

The Indian story

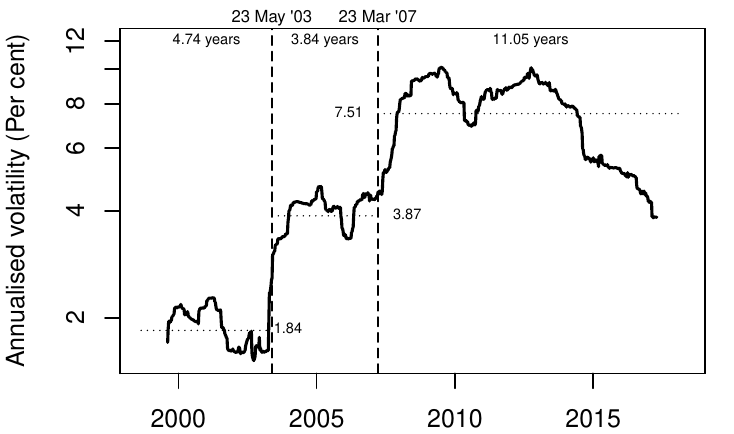

India's story is told in the graph above. Each point in the graph is the standard deviation of the USD/INR returns of the latest two years. We see an early period where we had a volatility of 1.84%. On 23 May 2003, exchange rate flexibility doubled, and we moved up to 3.87%. On 23 March 2007, exchange rate flexibility doubled again.

These changes, which were made by Dr. Reddy, were followed through by Dr. Subbarao with the policy of non-action on the currency market. RBI vacated the currency market, and the exchange rate was determined by supply and demand. As the graph shows, these gains were unfortunately reversed in the following years. We have now gone back to the conditions prevalent in 2003-2007.

Gains from exchange rate flexibility

Why is an exchange rate that fluctuates, in response to market forces, important?

- Dealing with shocks. When times are good, capital flows into India, and if we let the exchange rate appreciate, this stabilises a boom. When times are bad, capital leaves India, and if we let the exchange rate depreciate, this stabilises a bust. Exchange rate flexibility counteracts macroeconomic fluctuations.

- Moral hazard. When the exchange rate is more flexible, cross border activities tend to be layered with more private currency risk management. When RBI does currency risk management, this is free protection for private persons who tend to then leave currency risk unhedged. But big currency move do inevitably come about - no matter what RBI does - and they impose more damage upon parties who were not prepared for this move. A stable exchange rate thus lulls people into complacence, and then the damage caused by a large move is greater. It is better to have a large number of small changes in the exchange rate, i.e. an exchange rate that fluctuates all the time.

- Clarity of purpose. It is possible to give the central bank the objective of a stable exchange rate to the US dollar. As an example, Hong Kong has done this. But as a consequence, the central bank then loses control of domestic monetary conditions. India correctly chose a different path: From 2015 onwards, RBI has the formal objective of delivering 4% CPI inflation. Once this objective is written down (first in the Agreement and then in the Act), the focus of RBI has to be upon domestic monetary conditions. Buying or selling dollars means injecting or withdrawing rupees in the local money market, which interferes with domestic monetary conditions. Exchange rate management conflicts with domestic monetary policy.

- The potency of the central bank. The major problem for RBI in inflation targeting is the fact that as of today, monetary policy is fairly ineffectual. Exchange rate flexibility will increase RBI's potency. When the MPC raises rates, more capital will come into India, a floating exchange rate will appreciate, which makes traded goods cheaper, and reduces inflation. RBI should want to have greater influence upon domestic monetary conditions.

Looking forward

The Indian economy and the world economy face a variety of geopolitical and economic risks. There will surely be a next rough patch. Fighting a rupee depreciation under those conditions can be rather unpleasant.

As an example, in 2013, a small problem of a weakening rupee was converted into a big problem through policy mistakes. India chose to fight the rupee depreciation by raising the short term interest rate by 440 basis points, and a series of other harsh measures. These measures did not deliver a material impact upon the exchange rate and delivered a body blow to the economy at the worst possible time. This is the sort of risk that we run under the 2003-2007 arrangement, which was what motivated its reform by Reddy and Subbarao.

An exchange rate that is not volatile is soothing to the superficial mind. The wise approach is to obtain economic and financial stability by having an exchange rate that fluctuates.

Back up to Ajay Shah's 2018 media page

Back up to Ajay Shah's home page