The reconfiguration of global trade and FDI

Business Standard, 22 January 2024

The first and second globalisations

The `second globalisation' featured unconditional access for the periphery to the advanced economies that are the core of the world economy. The `third globalisation' makes this access more conditional on foreign policy and military alignment. New data shows the magnitude of the third-globalisation reconfiguration of trade and FDI. These developments present interesting puzzles for Indian foreign policy. Strategy thinking in firms needs to incorporate these considerations.

Many people think of globalisation as a modern phenomenon. In the good old days, however, governments did not interfere with the natural freedoms of the people: there were no restrictions upon the cross-border movement of goods, services, labour, capital or ideas. The limitation in that age was the costs associated with geographical distance. The first globalisation was the golden age from the Suez Canal (1869) to the First World War (1914), where the steamship, the telegraph and the Suez Canal resulted in a great surge of cross-border activity. The 20th century saw the rise and fall of nationalism. By the early 1980s, some measures of cross-border activity were back to 1914 levels. The technologies of telecommunication, container ships, wide body aircraft, and modern finance all came together to yield unprecedented levels of cross-border activity.

In the heyday of the second globalisation, the core gave complete access to their economic and technological might, even to countries who were prickly or hostile. The core understood the economic logic of unilateral opening up. Weaker policy teams were suspicious, and viewed cross-border freedoms for their people as something for the state to negotiate. There was an optimistic view in the core, that trade was civilising, that every country was going to surely become a nice liberal democracy. There was thus a benign approach to transferring knowledge to hostile nations.

The third globalisation

In recent years, there has been an upsurge of limitations upon cross-border activity in the core. The period from 2018 onwards is `The third globalisation' [Column in the Business Standard, 19 September 2022], [Everything is Everything Ep 17, 20 October 2023]. In the third globalisation, access to the core is given in more limited ways for countries that have a hostile foreign policy and military stance. The bulk of global GDP is in the core. They do full globalisation with each other, but they impose limitations upon hostile nations.

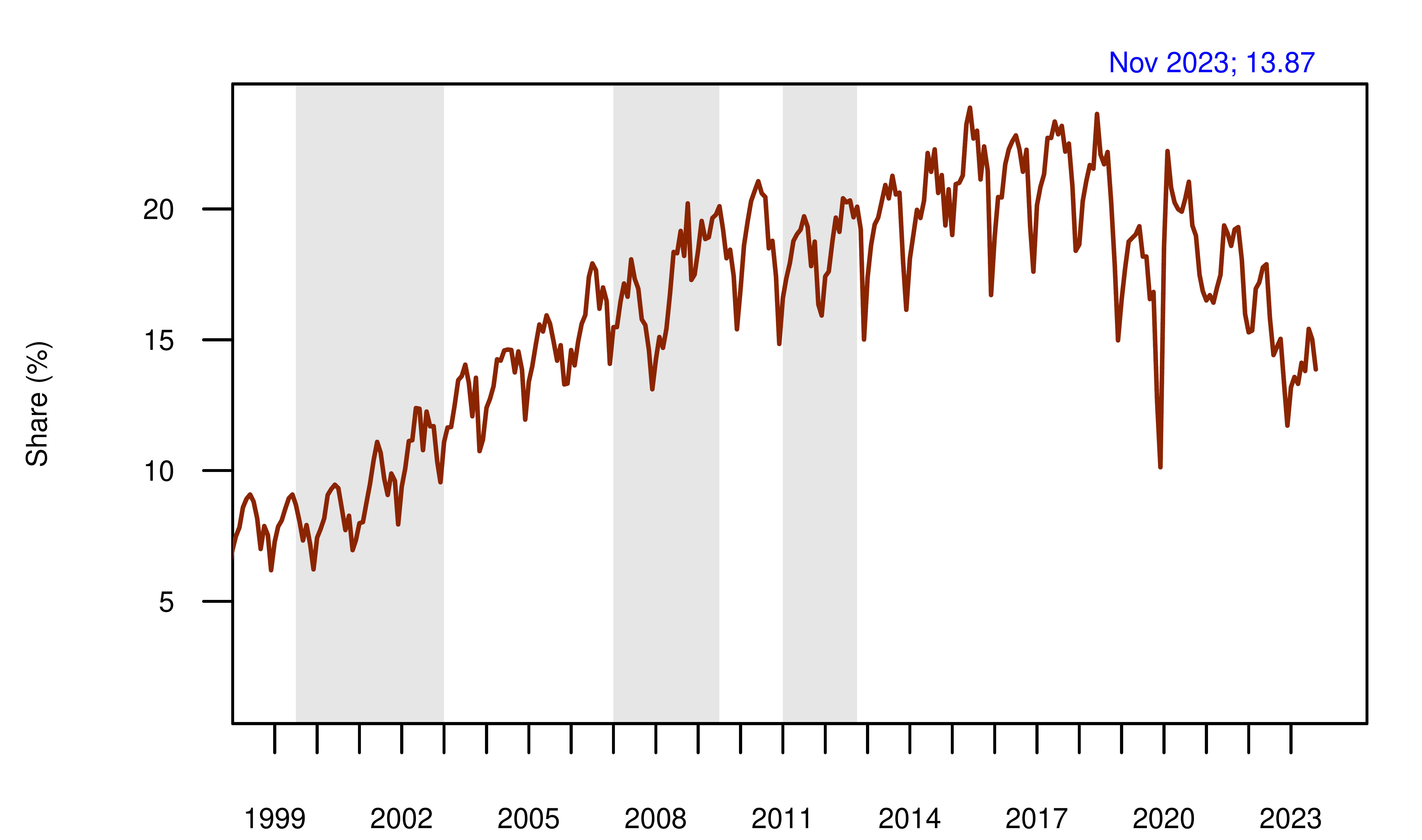

The graph shows the share of China in the goods+services imports of the US. This share grew dramatically from about 7 per cent to a peak of about 22 per cent. From about 2018 onwards, this share has dropped sharply. It is now back to the 2003 level of about 14 per cent. Xi Jinping's strategy has taken China back to where they were about 20 years ago. For a sense of scale, the present Indian share in US imports is at 2.61 per cent. China's decline over six years is 2.7 times bigger than the entire Indian exports to the US today.

Trade and FDI patterns in the third globalisation

A new paper from McKinsey Global Institute, `Geopolitics and the geometry of global trade', 17 January 2024, offers insights into the third globalisation. They bring together updated trade data with a technique from the field of international relations. The foreign policy alignment between two countries is measured by the extent to which they vote alike at the United Nations, for votes that are defined by the US Department of State as being `important'. Using this measure, each country pair is assigned a `geopolitical distance' ranging from 0 to 10. For example, the distance between the US and South Korea is 2 and the distance between Germany and Russia is 9.

The paper finds that the bulk of world trade happens between countries at the distance of about 3.5, the exception being China which does a lot of trade at a distance of about 5.5. Global trade was reconfigured in the 2017-2023 period reflecting the third globalisation. The trade-weighted geopolitical distance declined for some important countries: China (-4%), US (-10%), Germany (-6%) and UK (-4%). This trade reconfiguration is not complete. Today's FDI flows predict tomorrow's trade flows. FDI into China has dropped by 70% and FDI into Russia has dropped by 98%. Hence, it is likely that the third-globalisation reconfiguration of trade will run deeper in the future.

For India, there is a substantial trade engagement with China, which needs to be treated with respect as any sudden disruption would be counter-productive. For the rest, the bulk of the overseas engagement of the people of India -- on goods, services, people, capital, ideas -- is with the core. Hence, the interests of India lie in being a status quo power, that will work with the core and try to obtain economic growth in the coming century. The interests of the people are likely to gradually percolate into the state. There may be a gradual evolution of foreign policy and military strategy, to reflect the interests of the Indian people in this third-globalisation policy landscape of the core.

Implications for firm strategy

Policy levers are controlled by governments, but FDI and trade happens between private companies. The reconfiguration described above is about the rational responses of global firms to the changing world, and not central planning by officials. In the second globalisation, firms used to ignore the risks of engaging into undemocratic countries. They got their fingers burned, and are now rethinking their global operations.

Many firms are autarkic and do not care about international economics. But good firms export and the best firms do outbound FDI. Hence, the most important Indian firms are exuberantly connected into globalisation. Strategy thinking at these firms needs to bring a better understanding of the political system in various countries, the risks associated with doing business in undemocratic countries, and the evolving rules of the game that are being established by the core.

Back up to Ajay Shah's 2024 media page

Back up to Ajay Shah's home page